Mastercard Fees on Gambling Deposits: Every Charge Line Decoded

The receipt with five fees on a single deposit

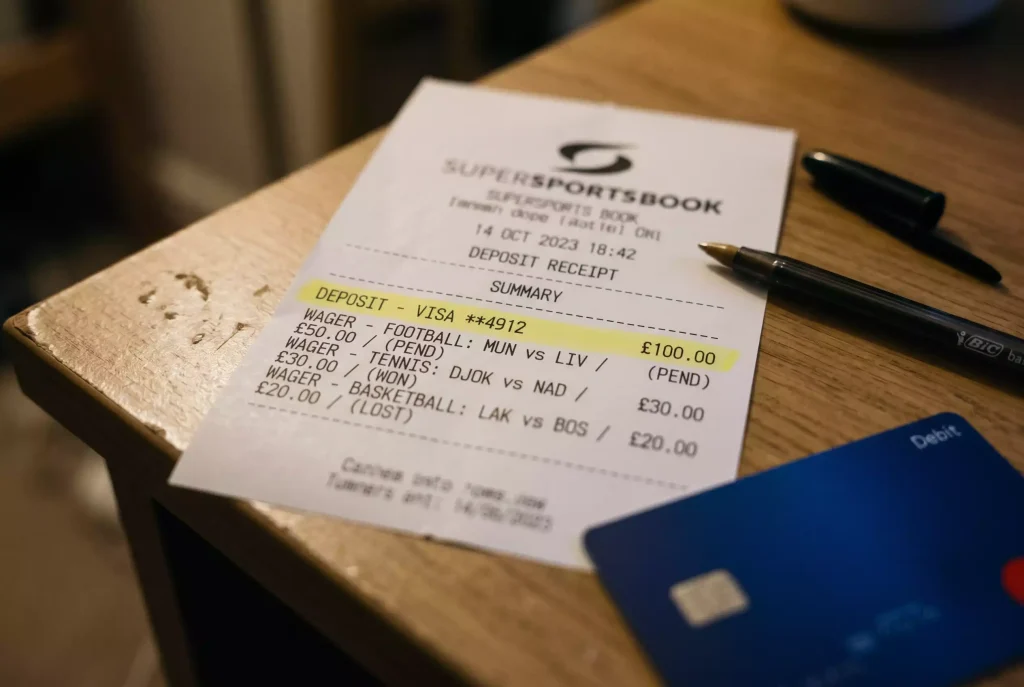

A reader forwarded me a statement last year showing a single $200 sportsbook deposit that had produced five separate fee-adjacent lines across his account. There was the deposit itself. There was a $10 cash-advance fee from the issuer. There was a $3 foreign-transaction fee. There was a currency conversion markup embedded in the exchange rate the issuer used. And there was a separate $4 deposit fee the operator charged. The cumulative cost of depositing $200 was $217 against a useful $200 of play balance — a 8.5 percent overhead on a single transaction, before any bet was placed.

The industry-level view helps calibrate this. As the American Gaming Association’s leadership has put it, legal commercial gaming in the US has delivered exceptional results for consumers, operators, and communities, with record revenues and tax contributions demonstrating the broad appeal of regulated gaming markets. That view is true at the aggregate level. At the individual-deposit level, the fee stack can quietly erode the bettor’s effective stake in ways that are rarely explained. This piece walks through every possible fee line on a Mastercard gambling deposit in 2026 — the flat operator deposit fee, the foreign-transaction charge, the currency-conversion markup, the issuer-added fees, and how to calculate the true cost of a deposit before you confirm.

The flat deposit fee by operator

Most regulated sportsbooks do not charge a flat deposit fee on card deposits. Most of the major US operators absorb the card-processing cost as part of the cost of business. A minority of operators pass through a small flat fee, typically $1 to $5, on credit-card deposits specifically, or a small percentage on credit deposits while leaving debit deposits fee-free.

The pattern is consistent across regulated markets. UK and Australian operators, where credit-card gambling is banned and all deposits flow through debit rails, almost never charge a deposit fee. US operators, where credit cards are still in play, split roughly 70/30 between absorbing the cost and passing through a small fee. Offshore operators are more variable — some charge nothing, some charge 3 to 5 percent on credit-card deposits to cover their higher processor costs.

The disclosure of the fee varies. Well-designed cashiers surface the fee before the deposit is confirmed, showing the bettor the exact amount they will be charged and the amount that will be credited to their account. Less-well-designed cashiers bury the fee in small print or disclose it only on the confirmation screen after the card details are entered. The practical rule is simple: if the cashier does not show the fee clearly, ask support before depositing.

A persistent reader question is whether the flat fee is negotiable. The honest answer for regulated operators is no — the fee is built into the payment processor integration and applies to all cardholders equally. For offshore operators the answer is sometimes, particularly for VIP accounts with large deposit histories, but the effort required to negotiate is rarely worth the handful of dollars saved per deposit.

The foreign-transaction fee

Foreign-transaction fees apply when a Mastercard is used at a merchant based in a different country from the card’s issuer. The fee is charged by the issuer to the cardholder, typically 1 to 3 percent of the transaction amount, and it appears as a separate line on the cardholder’s statement.

The trigger for the fee is the merchant’s processing location, not the bettor’s physical location. A US resident depositing at a US-licensed sportsbook does not pay a foreign-transaction fee regardless of where the bettor is physically located. A US resident depositing at an offshore operator registered in a different country pays the fee because the acquirer processing the transaction is foreign.

EU-domestic debit cards face a decline rate of 12 to 22 percent in iGaming, while EU cross-border transactions face 25 to 40 percent — numbers that illustrate the broader pattern where cross-border gambling transactions sit in a higher-friction category. The foreign-transaction fee is just one piece of that friction; declines, currency markups and timing delays all compound.

Some Mastercard products — typically premium travel cards or certain fintech cards — waive foreign-transaction fees as a product feature. For bettors who regularly use offshore operators, the product choice can materially reduce the overhead. For the full picture of how foreign-transaction charges actually accumulate on cross-border sportsbook deposits, including the network-level FX treatment and the issuer markup on top, the detailed audit sits in this piece on Mastercard foreign-transaction charges at offshore sportsbooks.

Currency conversion markup

When a bettor deposits in one currency at an operator that settles in a different currency, a conversion occurs — and the exchange rate used for the conversion carries a markup over the network’s mid-market rate. Mastercard, with roughly 1.1 billion credit cards in circulation globally representing a 32 percent share of the credit-card market, runs a visible network exchange rate that is close to but not identical to the mid-market rate.

The markup has two tiers. The first tier is the network’s own markup, typically 50 to 100 basis points over the mid-market rate. This is baked into the exchange rate the issuer applies to the transaction and is not disclosed as a separate fee. The second tier is any additional markup the issuer charges on top of the network rate — some issuers add another 50 to 300 basis points, others apply the network rate as-is.

The cumulative effect on a cross-border deposit can be meaningful. A $100 deposit at a EUR-settling operator might use an exchange rate that is 2 to 4 percent worse than the mid-market rate, which is effectively a 2 to 4 percent hidden fee that never appears as a separate line. The cardholder sees the deposit amount in their home currency and the effective rate is embedded in that conversion.

Some issuers show the exchange rate used on the statement. Others do not. Where the rate is shown, the cardholder can compare it to the mid-market rate for that date and calculate the markup. Where the rate is not shown, the markup is effectively unknowable without asking the issuer directly — and most frontline customer service representatives do not have the information at hand.

Issuer-added fees

On top of interchange (which the cardholder never sees) and foreign-transaction charges (which they do), some issuers add their own fees on specific card products that stack on top of a gambling deposit.

The most common is the cash-advance fee on credit cards, which I covered in detail in the cash-advance article in this series. A gambling MCC coded as cash-advance triggers a flat fee of 3 to 5 percent or a $10 minimum, plus daily-accruing interest at a higher APR than purchase transactions. For a single deposit held on balance for more than a month, the combined fee and interest can exceed 10 percent of the original stake.

Some premium cards have annual fees that are rationalised against reward structures; gambling transactions often do not earn rewards on the same basis as normal purchases, which effectively raises the annual fee’s cost on gambling-heavy card use. This is not a per-transaction fee but it is part of the total cost of using a specific card for gambling spending.

Certain prepaid Mastercards carry per-load fees or monthly maintenance fees that eat into the deposit balance independent of the gambling transaction itself. A $100 prepaid card with a $5 load fee provides $95 of gambling balance regardless of how the deposit is processed, and this is worth accounting for when comparing prepaid against debit.

Finally, a handful of cards charge per-transaction fees on any transaction above a certain velocity threshold. A card that charges $1 per transaction after the first ten each month will add up meaningfully for a bettor who makes small frequent deposits. This is less common in 2026 than it was a decade ago, but it persists on some subprime and rebuild-credit products.

How to calculate the true cost of a deposit

The practical bettor’s question is: what will a $200 deposit actually cost? The calculation is more tractable than it looks.

Start with the deposit amount. Add the operator’s flat deposit fee if any (check the cashier disclosure). Add the issuer’s cash-advance fee if the card is credit and the issuer codes gambling as cash-advance (check the card agreement or the first statement). Add the foreign-transaction fee if the operator is foreign (check the card agreement). Add the currency-conversion markup if currencies differ (assume 2 to 4 percent over mid-market). Add the carrying interest if the balance is not paid in full promptly (cash-advance APR at daily accrual).

For a domestic bettor using a domestic debit Mastercard at a domestic regulated operator, the true cost of a deposit is almost always zero beyond the deposit amount itself. No cash-advance treatment, no foreign-transaction fee, no conversion markup, and most operators absorb any interchange pass-through. The fee picture is clean.

For a domestic bettor using a credit Mastercard at the same operator, the cost depends on the issuer’s gambling MCC treatment and how quickly the balance is paid. If the issuer treats gambling as a normal purchase and the balance is paid by the statement date, the cost is zero. If the issuer treats gambling as cash-advance, the cost is 5 to 10 percent of the deposit depending on carry duration.

For a cross-border deposit at an offshore operator, the cost stacks. 3 to 5 percent operator deposit fee plus 2 to 3 percent foreign-transaction fee plus 2 to 4 percent conversion markup plus any cash-advance overhead. A $200 deposit can easily cost $220 to $230 all-in, against the notional $200 of bankroll.

The rule of thumb worth internalising: the simplest deposits — domestic, debit, regulated — are the cheapest, and every added complication adds several percentage points of real cost. The cashier optics of “$200 deposit, $200 credited” hide a lot of variance underneath.