Mastercard Betting: A 2026 Payments Analyst's Full Breakdown

The first Mastercard deposit I ever traced end-to-end at a sportsbook was a AU$50 credit card top-up that died three times in forty seconds before the player gave up and walked. The operator had flagged nothing wrong. The issuer had flagged nothing wrong. And yet the authorisation message came back with a hard decline every single time. That was my introduction, nine years ago, to the specific strangeness of card payments in regulated wagering — a corner of the payments world where a transaction can look perfectly clean at every checkpoint and still fail at the last one.

I've spent those nine years working in payment risk and iGaming compliance, watching the same script play out across thousands of accounts in Sydney, Melbourne, London, New Jersey and Toronto. The script has a name among people who build these systems: the iGaming decline problem. Roughly 30 to 40 percent of card transactions at regulated gambling operators never make it through, compared with 5 to 10 percent in general e-commerce. That's not a glitch. It's the deliberate output of a risk stack that treats gambling as a category apart.

This breakdown is the version of the conversation I wish someone had handed me on day one. It covers MCC codes, issuer logic, decline anatomy, the fee stack, regulatory turns in the UK, Australia, the US and Brazil, and the security layers most players never see. Written from the payments side, not the affiliate side.

The Short Version for Readers Who Only Have a Minute

- Card decline rates in iGaming run 30 to 40 percent, versus 5 to 10 percent in ordinary e-commerce. Most of that is category-level, not you.

- MCC 7995 is the global gambling code, MCC 7801 is the narrower US-regulated code, and that four-digit tag drives most approval outcomes.

- US sports-betting GGR hit a record 16.96 billion dollars in 2025, on a handle of 166.94 billion dollars, with 84 percent of bets placed on mobile.

- The UK, Australia since 11 June 2024, and Brazil under the 2026 rollout have all banned credit-card funding of online wagering.

- Withdrawals use Mastercard Send on eligible debit cards only; credit cards generally get paid out via ACH fallback.

How Mastercard Actually Moves Your Money to a Sportsbook

Most players picture a Mastercard deposit as a single button press. On the backend it's a four-party conversation that finishes in under two seconds, and every one of those parties can veto the transaction. Understanding who's in that conversation is the difference between guessing why something failed and knowing.

When you type a card number into a sportsbook cashier, the operator's payment page hands the details to an acquirer — the bank or processor that holds the merchant account on the gambling side. The acquirer packages the authorisation request with a Merchant Category Code attached, routes it across Mastercard's global switching network, and delivers it to the issuer — the bank that wrote you the card. The issuer looks at its own risk model, your available balance, your recent activity and the MCC, then either approves or declines. That answer travels back the same way in reverse.

The four parties on every Mastercard bet deposit

Cardholder, issuer, Mastercard network, acquirer and the sportsbook merchant itself. Mastercard doesn't lend you money or hold funds — it's the switch. The network moves authorisation messages and, later, settlement files. The issuer carries the credit or debit risk. The acquirer carries the merchant risk. A decline can come from any node in that chain, and the decline message you see on the cashier page almost never tells you which one made the call.

Issuer — the bank or credit union that issued the Mastercard in your wallet. In an Australian context that's usually CommBank, Westpac, NAB, ANZ or one of the mutual banks. The issuer owns the risk on a credit line and signs off on every authorisation.

Acquirer — the bank or payments processor that holds the sportsbook's merchant account and physically routes the deposit request into the network. Gambling-licensed acquirers are a small subset of the wider acquiring market. High-risk specialists like Worldpay's gaming division or Nuvei tend to sit in this seat.

The architecture matters because Mastercard runs on 2.95 billion issued cards worldwide and holds 32 percent of the global credit-card market behind Visa. That scale is exactly why the network doesn't make policy calls on individual transactions. It publishes rules in the Quick Reference Booklet — the dense document that defines how gambling merchants must be coded, how chargebacks work and which regions permit which card products — and then leaves the day-to-day yes-or-no to the issuer on one side and the acquirer on the other. If you want to know why a deposit failed, those are the two phone calls to make.

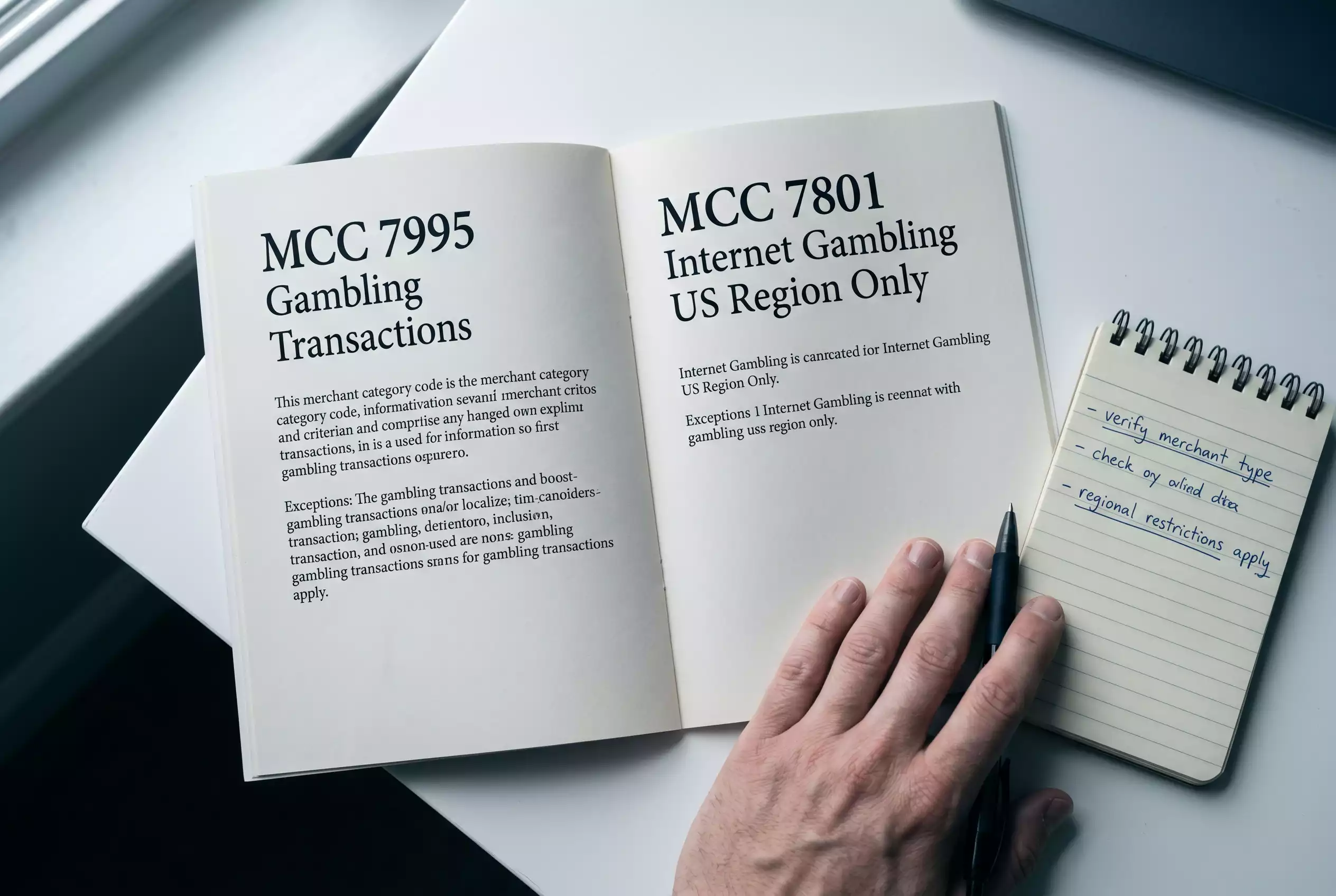

MCC 7995 and MCC 7801: The Four Digits That Decide Everything

If I could only explain one thing to every player who asks me why their card keeps getting rejected, it would be this: the sportsbook doesn't describe itself to your bank in words. It describes itself in four digits. And those four digits carry most of the decision.

MCC — Merchant Category Code. A four-digit classifier that every acquirer is required to assign to every merchant it onboards. It tells the issuer what kind of business is asking for money, and lets the issuer apply category-level rules, interchange rates and decline logic. There are around 800 MCCs in the current Mastercard schedule; gambling uses exactly two of them.

The first is MCC 7995 — Gambling Transactions. This is the global default for any betting, lottery or casino merchant. If you deposit to an offshore sportsbook from Sydney, or a UK high-street book, or a Maltese casino, the authorisation almost certainly arrives at your issuer tagged 7995. That single code triggers a cascade of controls: credit-card bans in the UK and Australia, cash-advance treatment at many US banks, higher interchange, harder velocity checks, and in some cases an automatic decline rule regardless of balance.

The second is MCC 7801 — Internet Gambling, US Region Only. Mastercard created this code specifically for US-regulated operators after the post-PASPA rollout began in 2018, and reserved it for licensed sportsbooks and iGaming sites operating inside states that have legalised the product. An issuer seeing a 7801 knows two things immediately: the merchant is domestic, and the merchant is state-licensed. That context often unlocks approvals that a raw 7995 would never get.

MCC 7995 vs MCC 7801 at a glance

MCC 7995 applies globally to gambling transactions and is the default code most sportsbooks inherit. MCC 7801 is a narrower code restricted to US-regulated internet gambling and was introduced as the US market reopened. The practical effect on approval is large: a US domestic debit card seeing a 7801 from a licensed New Jersey operator sits in a very different risk bucket than the same card seeing a 7995 from an offshore site. The code does not change what the merchant sells. It changes how every issuer in the chain reads the transaction.

The gap between those two codes is where the decline numbers live. The industry-wide iGaming decline range — the 30-to-40 band I opened with — isn't uniform inside it. That gap shrinks substantially for 7801 traffic and widens for 7995 cross-border traffic. On EU domestic debit the decline rate sits around 12 to 22 percent; cross-border debit runs 25 to 40 percent. The coding sits underneath every one of those numbers.

For an Australian cardholder trying to deposit at an offshore book, the 7995 tag is one half of the problem. The other half — the June 2024 credit-card ban — sits on top of it, and I'll come back to that in the regulatory section.

Where the Money Sits Right Now

Walk through a major Australian betting hub on a Saturday afternoon in NRL finals season, watch the phone screens, and you'll see roughly the same scene replayed in every booth in Las Vegas, every pub near Old Trafford and every living room in Ontario. The sports-wagering market has become a global, card-driven and overwhelmingly mobile machine, and the scale has shifted in ways most players underestimate.

16.96 billion

US sports-betting GGR in 2025, a 22.8 percent jump year on year

166.94 billion

US legal handle in 2025, up 11 percent year on year

78.72 billion

Total US commercial gaming GGR in 2025, across casino, sports and iGaming

84 percent

Share of US sports bets placed on mobile in 2025

Those are US figures because that's where the transparent reporting is cleanest. The Australian market isn't small — the country sits in the top three per-capita wagering markets globally — but the domestic regulated books report on different cycles and the comparable public numbers trail by a few quarters. What matters for a payments analyst isn't the top-line revenue; it's the mix underneath.

Cards still run the deposits side of that mix. Across regulated markets, credit and debit cards sit at or near the top of the deposit-method league table: around 60 percent in the US, 55 percent in Southern Europe, 45 percent in UK retail online wagering where debit still dominates post-ban. The 2024 global online-gambling card volume — credit and debit combined across all gambling verticals — cleared 66 billion dollars. Cards don't win at gambling merchants because everyone loves them. They win because every other rail has a rougher edge for somebody, and because the tokenised mobile card has quietly become the universal deposit instrument of the industry.

That volume is the backdrop to everything else in this article. When I talk about decline rates, fees, fraud controls and regulatory turns, I'm talking about the plumbing that sits underneath a flow now measured in tens of billions of dollars a month.

What Happens When You Press "Deposit"

A deposit that works feels like nothing. A deposit that fails feels like an ambush, usually at the worst possible moment, and almost always without a useful error message. The reason most players can't diagnose their own deposit failures is that the cashier page is the last page in a pipeline that started several seconds earlier, and the vocabulary the page uses is carefully designed to tell you nothing.

In mechanical terms, a Mastercard deposit at a sportsbook is a standard card-not-present authorisation. The cashier captures the PAN, expiry and CVV, tokenises them at the payment gateway, sends an auth request through the acquirer to the network to the issuer, and waits for a response code. If the response is an approval, the cashier credits your player wallet immediately — that's the "instant deposit" experience. If it's a decline, you see a polite message that almost never names the real reason.

Illustrative deposit example, not a real operator figure

Suppose you deposit 100 units on a Mastercard credit card at a sportsbook that charges no player-side deposit fee. The sportsbook credits 100 units to your wallet instantly. The card statement, if coded as a purchase, shows a 100-unit charge. If your issuer codes the same transaction as a cash advance, the statement shows a 100-unit charge plus a cash-advance fee, often 3 to 5 units, plus interest accruing immediately at the cash-advance APR. Nothing on the sportsbook cashier tells you which one just happened.

Why "the deposit went through" and "the deposit didn't go through" can both be true in the same minute. Authorisation holds are not settlement. An issuer can approve an auth, place a hold on your available balance, and then kill the hold in a separate risk-pass seconds later. The hold vanishes, the funds never land at the operator, and you're left refreshing the cashier page wondering what happened. This is the single most common silent failure mode I see.

The detailed deposit flow — limits by operator, credit-vs-debit approval math, how long settlement actually takes, the reversal window, and the failure modes beyond the simple decline — sits in a dedicated breakdown I wrote on how the Mastercard deposit flow really works at sportsbooks. For this pillar, the mental model is enough: a card deposit is one authorisation against one issuer, and everything you care about happens in the 400 milliseconds between the cashier press and the response code.

Getting the Money Back: The Push-to-Card Reality

Here's the asymmetry that catches every new card-paying player at some point: your Mastercard can push money into the sportsbook in two seconds, but getting it back the same way is a completely different payment rail with different rules, different eligibility and different failure modes. Deposits use a purchase authorisation. Withdrawals, when they work, use something called an Original Credit Transaction — in Mastercard's branding, Mastercard Send.

Mastercard Send is not a separate card. It's a network service that lets a merchant push funds directly to an eligible debit or prepaid card using the same 16-digit number the player used to deposit. The issuer has to participate, the card has to be eligible — credit cards generally are not — and the acquirer has to be enabled for push payments. All three conditions lining up is rarer than most players expect, which is why "card in, bank transfer out" has quietly become the industry's default payout shape.

When Mastercard Send does work, the experience is genuinely fast: funds usually land on the card within thirty minutes of the sportsbook approving the payout, sometimes under five. When it doesn't work — because the card is a credit product, or the issuer hasn't turned on push-to-card, or the operator's acquirer hasn't enabled Send — the operator quietly reroutes the payout to ACH, a bank transfer or in rare cases a paper cheque. You still get paid. You just wait longer. The critical difference between deposit and payout paths, from a risk-control view, is that a push to a compromised card is irreversible: the fraud-detection weight moves from the merchant-acquirer side to the issuer side and happens before the push leaves, not after.

Everything that sits underneath that summary — which US operators reliably support Send, what to do when the push fails, push-to-card eligibility by card type, and why some books won't even show the card as a payout option — I've unpacked in the dedicated guide on Mastercard sportsbook withdrawals and the Send rail. For the pillar, just remember: deposit path and withdrawal path are not the same path, even when the card number is the same.

Why Your Card Says No: Declines, Velocity and the Fraud Layer

A tier-one US sportsbook I worked with once pulled me into a review because their Mastercard approval rate had dropped from 74 percent to 61 percent in a single week. No issuer had changed policy. No acquirer routing had flipped. The operator hadn't touched their risk stack. The culprit turned out to be a single Tuesday morning model update at one major card issuer that had retrained on a window of freshly labelled gambling fraud. Thirteen points of approval rate, gone, from a decision made in someone else's ML pipeline.

That's the shape of the decline problem in this industry. You're running on a network where three separate risk engines — issuer, acquirer, operator — can each independently reject a transaction, and none of them tells the others what they're doing. Layer on top of that the fraud backdrop, which has gotten materially worse.

The gambling-industry fraud rate climbed from 4.2 percent in 2022 to 7.6 percent in 2023 — an 80 percent increase in a single year. Around 4 percent of all login attempts on gambling platforms in 2023 were account-takeover attempts, and the industry collectively loses roughly one billion dollars a year to cyberattacks, with account takeover as the lead vector. That environment is the reason issuer risk scores on gambling merchants have been tightened everywhere in the last two cycles.

The practical result is a set of decline triggers that hit clean cardholders as collateral damage. Cross-border geography is the biggest one: if your card's BIN says Australia and the merchant's acquirer says Curaçao, you're in the highest-risk bucket the issuer has. Velocity is second: three deposit attempts in ninety seconds looks like card-testing to a fraud model, even when it's just you retrying after a decline. AVS mismatches, even minor ones, strip off another five to ten points of approval. And, of course, the MCC itself sits behind every one of those checks.

For Australian players post-June 2024, an additional filter runs before any of this: credit-card BINs for Australian gambling transactions are now blocked upstream by the operator's regulated acquirer under domestic law, and that block happens before the issuer ever sees the request. The full diagnostic workflow — how to read the decline reason codes, which banks are tightest on gambling, what to change on your second attempt and when to stop trying — sits in the dedicated walkthrough on why your Mastercard gets declined at a sportsbook and how to fix it.

The Fee Stack You Never See on the Cashier Screen

Ask a betting mate what a Mastercard deposit "costs" and they'll usually say nothing, because the operator doesn't charge a player-facing fee on the cashier page. That answer is technically correct and substantively wrong. The fee stack is real, it's stacked, and at least part of it ends up on your statement even when nothing looks like a fee at the sportsbook.

There are three layers worth knowing. Interchange is the first: the fixed percentage the issuer keeps when it settles the transaction with the acquirer. Gambling interchange — the 7995 category — typically runs higher than the ordinary credit-card interchange band, because the scheme has priced the risk in. The acquirer adds its own markup on top, and the operator absorbs both out of its gross margin. So far, nothing touches the cardholder directly.

| Fee type | Who pays it | When it hits the player |

|---|---|---|

| Interchange | Operator via acquirer | Never directly. Embedded in merchant margin |

| Cross-border assessment | Operator, then sometimes passed on | When an issuer charges a foreign-transaction fee on the settlement country, usually 1 to 3 percent of the deposit |

| Cash-advance fee | Cardholder | Whenever the issuer codes the gambling deposit as a cash advance, typically 3 to 5 percent plus immediate cash-advance interest |

| Acquirer markup | Operator | Never visible to the player. Absorbed in operator economics |

| Flat per-deposit fee | Cardholder if applied | Rare on regulated US books. More common on offshore and grey-market operators |

Cross-border is where most Australian and UK players get the silent tax. If the sportsbook's acquirer settles in a currency or country different from your card's home, the issuer can apply a foreign-transaction surcharge even though the amount on the cashier was stated in your home currency. That surcharge arrives on the statement, not the cashier. The cash-advance problem is the other quiet killer. On cards coded 7995, around one in four US sports bettors reported their issuer treating at least one gambling deposit as a cash advance — with 24 percent of sports bettors using credit-card cash advances specifically to fund betting in 2025.

The headline for the player: zero at the cashier isn't zero on the statement. Read the statement before you argue the deposit was free.

The Security Layers Between Your Card and a Bookmaker

Is a Mastercard actually safer for betting than, say, a direct bank transfer or a crypto rail? A cybersecurity expert quoted in an AARP piece last year put the position as bluntly as anyone in the field: stick to credit cards or trusted digital wallets with fraud protection, and avoid wire transfers, crypto and peer-to-peer payment apps that don't offer buyer protection. That advice holds for betting specifically, not just for shopping, and the reason is the chain of defensive layers that now sits between a Mastercard PAN and a sportsbook cashier.

The layered security stack on a modern Mastercard deposit

3D Secure 2 runs an out-of-band authentication handshake between the cashier and the issuer — typically a push notification to your banking app — before the authorisation even goes to the network. Tokenisation replaces the real 16-digit PAN with a device-specific token that's useless if intercepted. Click-to-Pay standardises the guest-checkout flow so you're not typing the card number into yet another merchant form. Zero Liability policy caps cardholder exposure on unauthorised use. And behind all of that, Mastercard's Decision Intelligence Pro platform now identifies compromised cards roughly twice as fast as the prior model.

The practical effect is that an unauthorised deposit on a tokenised Mastercard at a 3DS2-enabled sportsbook is, in most regulated markets, one of the safer consumer-payment events you can construct. The dispute rail is well-defined, Zero Liability is enforceable, and the fraud-detection layer is genuinely fast. Contrast that with a reversed crypto transfer to the wrong address — there is no rail.

Safer doesn't mean safe from your own risk profile, though. A card stored in a mobile wallet, protected by biometric passkeys and authenticated through 3DS2 is a hardened attack surface on the technical side. It's still the same card that, if you chase losses, will accept another deposit request an hour later. The security stack protects you from fraud. It does not protect you from yourself, and conflating those is where a lot of bad decisions start. The end-to-end safety picture, including dispute mechanics, 3DS2 friction, tokenisation eligibility by card product and chargeback rights on gambling debits, sits in the dedicated breakdown on Mastercard betting safety, fraud protection and the chargeback question.

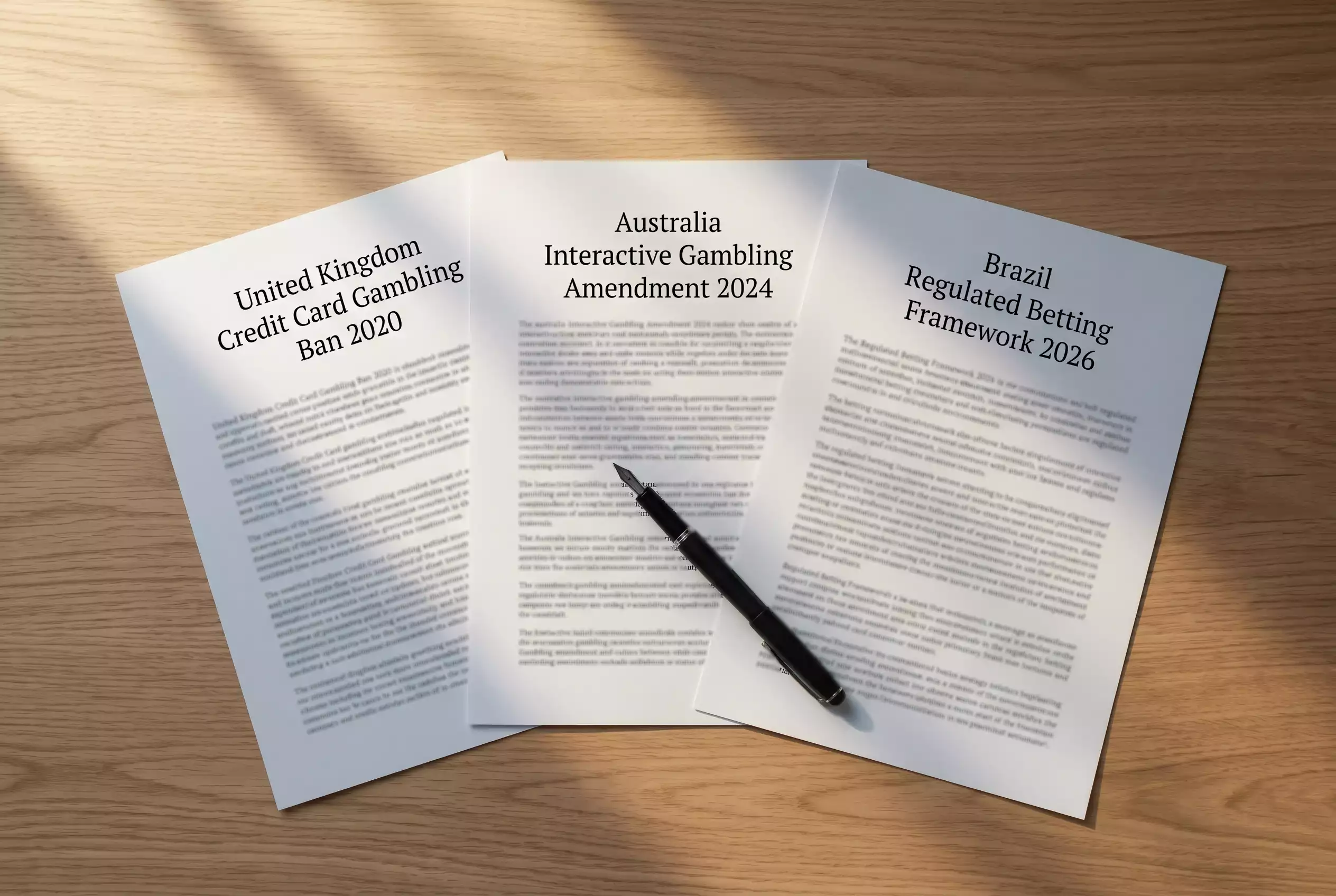

Four Jurisdictions, Four Different Answers

The single most surreal meeting of my career was in June 2024, sitting across from the compliance team of a regulated Australian wagering operator, watching them rewrite thirty-one percent of their cashier in seventy-two hours. The trigger was section 61 of the Commonwealth amendment. The deadline was non-negotiable. And every single credit-card deposit path in the product had to be ripped out and replaced before the 11 June go-live. Regulation in this industry doesn't arrive gradually. It arrives on a specific Tuesday, and the payments stack has to be ready.

| Jurisdiction | Credit-card gambling status | Key date | Enforcement mechanism |

|---|---|---|---|

| United Kingdom | Banned for all GB-licensed online and offline gambling | 14 April 2020 | UK Gambling Commission licence condition. Applies to all operators holding a GB remote licence |

| Australia | Banned for online wagering. Credit cards, credit-related products and digital currency prohibited as funding sources | 11 June 2024 | Interactive Gambling Amendment (Credit and Other Measures) Act. Fines up to AU$234,750 per breach enforced by ACMA |

| United States | Permitted at federal level. State-regulated. Many issuer-side restrictions in practice. MCC 7801 in use for domestic regulated operators | Ongoing post-PASPA 2018 | State gaming commissions, issuer risk policy, Mastercard Rules |

| Brazil | Credit-card funding of regulated betting prohibited under the SPA framework | April 2026 regulatory cycle | Secretariat of Prizes and Betting. Part of the full regulated-market rollout |

The UK was first, in April 2020, when the Gambling Commission introduced an outright ban across all GB-licensed operators. The Commission's rationale was straightforward and the evidence base was public: among online gamblers who used credit cards to fund bets, 22 percent met the clinical threshold for problem gambling, with an independent evaluation putting the figure as high as 24 percent — more than double the 11 percent rate among players using alternative funding methods. The Commission framed the move as part of a multifaceted effort to reduce gambling harm, with consumer protection as the stated core.

Australia followed in June 2024, after a Commonwealth-led review that had been gathering weight for three years. The government's framing was plainer: Australians should not be gambling with money they do not have. The ban captures credit cards, credit-related products and digital currency as funding sources for online wagering, and ACMA enforces it with fines up to AU$234,750 per breach. Since the BetStop national self-exclusion register came online alongside the regulatory cycle, more than 22,000 Australians have registered themselves off. The US sits at the opposite end of this map — state-licensed, federally permitted, and running the only MCC code (7801) specifically built for regulated internet gambling. Brazil is the next major jurisdiction to close off credit-card funding, doing it inside a much newer regulated-market framework during the current 2026 cycle. Four jurisdictions, four different answers, one underlying card network.

Credit Cards, Problem Gambling and the Debt Ledger

The UK ban wasn't a theoretical policy. It was a response to a specific, measurable cluster of harm, and in the years since, the US data has filled in the picture in terrifying detail. One survey from 2025 found that 24 percent of American sports bettors had used a credit-card cash advance to fund bets, 16 percent had taken a personal loan for the same purpose, and 12 percent had resorted to payday lending. A further 30 percent attributed some of their personal debt directly to gambling, and 52 percent of that group were already carrying a credit-card balance from month to month. The credit-card-plus-sports-betting combination is not a neutral product.

The Debt.org coverage captured an NCPG leader's line on the specific danger of the credit-funded bet: you can spend "virtually any amount you want," which loads risk onto the gambler and the family around them, while chasing losses stays the default failure mode. It's a plain description of what credit mechanics do when paired with an instant-deposit cashier.

The scale of the underlying population is the part that doesn't make it into most betting articles. Around two million Americans meet the criteria for severe gambling disorder; another four to six million fall into mild or moderate categories. Roughly 8 percent of US adults, close to 20 million people, have reported at least one indicator of problem gambling behaviour "many times" in the prior year. Among men with gambling disorder, average accumulated debt runs between 55,000 and 90,000 dollars; for women, around 15,000. Twenty percent of problem gamblers file for bankruptcy as a direct consequence of gambling losses. Those are NCPG figures, and they are not improving on a trend line.

US helpline — National Problem Gambling Helpline

The NCPG operates 1-800-GAMBLER, a 24/7 confidential helpline that provides call, text and chat support in all fifty US states. For Australians, the equivalent national resource is Gambling Help Online at 1800 858 858. The UK service is GamCare on 0808 8020 133. These are not payment-industry resources. They exist because the payment industry's biggest external cost has, for two decades, been the downstream harm from products that deposit faster than they can be regulated.

I include this in a payments breakdown for one reason: the card is the instrument. When you're choosing between a credit-line deposit and a debit deposit, you're not just choosing an approval rate. You're choosing between an instrument that caps at your own money and one that doesn't. Every analyst in this industry knows which of those two shapes produces the call to the helpline.

When a Mastercard Isn't the Right Rail

Cards dominate deposit volume across regulated markets, as the earlier snapshot numbers make clear. But "dominates on volume" is not the same as "is always the best rail for you." Whenever a Mastercard deposit fails repeatedly, or whenever a payout is quietly downgraded from Send to bank transfer, I tell players to treat the other rails as genuine competitors, not as fallback stopgaps.

| Rail | Speed in | Speed out | Fee profile | Works well for |

|---|---|---|---|---|

| Play+ prepaid card | Instant | Minutes to hours | Low operator-funded | US players who want card-like UX with a predictable payout rail |

| PayPal | Instant | Instant to 24 hours | Low to none for players | Symmetric in-and-out flow where supported |

| Skrill | Instant | Hours | Low, currency-dependent | Cross-border European wagering |

| ACH bank transfer | Minutes to 1 day | 1 to 5 days | Free or flat small fee | Large deposits and cleanest audit trail |

| Cryptocurrency | Minutes | Minutes | Network fee, no chargeback rail | Unregulated markets only. No dispute rights |

The honest summary: Play+ and PayPal are the closest like-for-like substitutes for a Mastercard in US regulated wagering, ACH is the cleanest for large balances and the easiest to document when someone asks where your bankroll came from, and crypto is a rail you choose only if you understand you're giving up the dispute mechanics that make card payments recoverable. The 2024 global card volume into sports betting and online gambling was still the biggest line on the method chart, but the growth on Play+ and on real-time bank rails has been steeper than anything happening on cards.

How Tier-One Books Handle the Same Card Differently

A reasonable question at this point: if the MCC is the same, the network is the same and the issuer is the same, why does the same Mastercard behave so differently across two tier-one books in the same US state? The answer is that the parts of the stack the operator actually controls are small, but the ones that are theirs make a visible difference on the cashier.

Tier-one US-regulated books — FanDuel, BetMGM, DraftKings and Caesars all exist in this category, all hold state licences in the jurisdictions where they operate, and all route Mastercard deposits under MCC 7801 — sit on different acquirers, different fraud-stack vendors and different internal risk thresholds. The cashier differences the player actually sees come down to a handful of variables.

| Variable | What it controls | Why it differs by operator |

|---|---|---|

| Minimum deposit | Floor on a single card transaction, typically 5 to 20 USD | Acquirer cost of a small auth vs marketing-funnel strategy |

| Maximum daily deposit | Ceiling on cumulative card deposits in 24 hours | Risk appetite and AML monitoring thresholds |

| Card payout support | Whether Mastercard Send is offered as a payout method at all | Whether the operator's acquirer is push-to-card enabled and whether the book has integrated Send |

| Reversible pending withdrawals | Whether a pending payout can be clawed back into the wallet | Retention design vs responsible-gambling policy |

| 3DS2 friction | Whether the issuer challenge pops on every deposit or only on flagged ones | Acquirer-level scheme elections and frictionless-flow economics |

That last variable is probably the most underrated. An operator that always forces 3DS2 challenges on card deposits will look slower on the cashier than one that opts for frictionless 3DS2 most of the time. Neither is wrong. They're expressing different risk tolerances. The full mapping of which regulated books reliably accept Mastercard in which jurisdictions, how the cashier behaves at each, and how to check acceptance before you fund, sits in the 2026 acceptance map of Mastercard-ready sportsbooks. I've deliberately written that one as a map, not a ranking — which books to choose is your decision, not mine.

The Card Isn't a Card Anymore, It's a Token on Your Phone

Nobody actually uses a plastic Mastercard to bet anymore. They use a token. The physical card in your wallet, if it's even still there, is a backup for the times Apple Pay doesn't load. That shift happened fast, and it's reshaped every part of the deposit experience the industry designs for.

Mobile betting accounts for 84 percent of all US sports bets placed in 2025. Among 18-to-34-year-olds, more than 85 percent of bettors use mobile apps as their primary platform. Contactless Mastercard payments — nearly all of them tokenised — hit 59.2 percent of all North American card transactions in the same year. Cards that are not on a phone, increasingly, are cards that are not getting used.

Tokenisation is the reason this shift has been safer than it should have been, statistically, given how much money now moves through it. When you add a Mastercard to Apple Pay or Google Pay, the wallet calls Mastercard's tokenisation service, which provisions a Device Primary Account Number — a 16-digit token that looks like a card number, is cryptographically bound to the specific device and the specific user, and is useless to anyone who intercepts it elsewhere. The real PAN never leaves the issuer. The merchant, including any sportsbook you deposit to, only ever sees the DPAN.

For a sportsbook cashier, that changes the risk picture materially. A DPAN can't be reused from a skimmed magstripe, can't be spun up in a card-not-present fraud attack the way a raw PAN can, and — when paired with biometric passkeys on the device — gets an authentication factor stronger than any static password. The approval rates I see on tokenised Mastercard deposits at tier-one operators routinely sit five to eight percentage points above the same card in its raw form.

Where Card Rails Are Heading Next

The online sports-betting market is forecast to climb from 51.91 billion dollars in 2025 to 173.45 billion by 2035, a compound annual growth rate of 12.82 percent. The card rails that move the money into and out of that market are not going to look the same in five years as they do now, and the direction of travel is already visible in the product roadmaps.

Three shifts matter. The first is the continued compression of the deposit flow. Click-to-Pay, guest-checkout standardisation and the gradual phase-out of manual CVV entry on tokenised cards are all pushing toward a cashier experience where "deposit" is a single biometric confirmation, nothing more. The second is the maturation of push-to-card as the default payout rail — Mastercard Send adoption is rising at every tier-one US book I've audited, and the cycle where ACH is the fallback is flipping toward ACH as the fallback to Send, not the default. The third is AI on the risk side, and it cuts both ways. A tech policy expert writing in Axios late last year warned that AI will "help sportsbooks fine-tune their odds — making them even less likely to lose," while the same class of models on the issuer and network side are already detecting compromised cards roughly twice as fast as their predecessors.

The American Gaming Association's leader described 2025 as delivering "exceptional results for consumers, operators, and the communities we serve," and that framing captures the regulated industry's posture coming into 2026. The card rail underneath that growth is getting faster, more tokenised and more aggressively risk-scored at the same time. Expect fewer visible declines at the cashier, more invisible risk decisions made upstream, and a shrinking window in which raw card numbers — as opposed to tokens — exist anywhere in the deposit flow.

Questions I Get Asked Every Week

Can I deposit with a Mastercard credit card at a US sportsbook?

In most US-regulated states, yes — subject to your issuer's own policy. The operator-side path is legal at federal and state level, and tier-one books route these deposits under MCC 7801, which is the friendliest coding a card deposit can get. The veto usually comes from the issuer. Several major US card-issuing banks apply category-level blocks on gambling MCCs regardless of state licensing, and some that allow the deposit will code it as a cash advance. The way to check is to run a small first deposit, then look at the pending statement line and the deposit-method acceptance list on the cashier before funding any size amount.

Can I withdraw my winnings back to my Mastercard?

Only on cards eligible for Mastercard Send, which in practice means most debit cards at participating issuers and essentially no credit cards. If your card is Send-eligible and the operator has enabled push-to-card, payout lands in minutes to an hour. If either condition fails, the book quietly routes the payout to ACH or a bank transfer and the wait stretches to days. The cashier rarely explains which path you're on — check the withdrawal method list on the operator's banking page before depositing.

Is there a flat per-deposit fee when I fund a sportsbook with Mastercard?

At most US-regulated tier-one books, no. At offshore and grey-market books, sometimes. The real cost is upstream: if your issuer codes the deposit as a cash advance, you pay a 3 to 5 percent cash-advance fee plus immediate cash-advance-rate interest. If the sportsbook's acquirer settles cross-border relative to your card, a foreign-transaction surcharge of 1 to 3 percent can land on the statement too. Zero at the cashier is not zero on the statement.

How fast are Mastercard deposits and withdrawals at sportsbooks?

Deposits are effectively instant when approved — the wallet credit hits within seconds of the authorisation. Withdrawals via Mastercard Send typically clear in 30 minutes or under, but only on eligible cards at enabled operators. A Send-routed payout that falls back to ACH usually arrives in 1 to 5 business days. The wildcard is the operator's internal review window, which can add anywhere from a few minutes to several hours on a first payout.

What is the difference between MCC 7995 and MCC 7801?

MCC 7995 is the global Gambling Transactions code — the default for any betting, lottery or casino merchant anywhere in the world. MCC 7801 is Internet Gambling, US Region Only, reserved for US-regulated online gambling operators. The practical effect is large: a US-licensed book coded 7801 often approves on cards that would reject the same deposit under 7995 from offshore. The MCC doesn't change what the merchant sells. It changes how every issuer in the chain reads the transaction.

Is Mastercard safer than e-wallets for sports betting?

In regulated markets, Mastercard sits at the top tier for consumer-protection strength alongside trusted digital wallets like PayPal. Zero Liability policy, 3D Secure 2, tokenisation and chargeback rights all apply on card deposits to licensed operators. E-wallets add an additional custodial layer between the card and the sportsbook, which some players find useful for budgeting and statement cleanliness. Both are materially safer than wire transfers or unprotected peer-to-peer payment apps for this specific use.

Which countries still allow Mastercard credit card gambling?

The United States federally permits it and leaves the details to state law. Canada permits it province by province, and most provincial regulators allow card funding. Most of continental Europe permits it subject to licence conditions. Banned outright: the United Kingdom since April 2020, Australia since 11 June 2024 for all online wagering, Brazil under the 2026 regulated-market rollout. Several US and EU jurisdictions have active reviews. The safest assumption is that the credit-card path is tightening globally, not loosening.

Running a Mastercard Deposit Like an Analyst Would

The working analyst's rule of thumb, after nine years watching this rail in every configuration it comes in: treat a Mastercard deposit at a sportsbook as an ordinary card transaction with three extra layers of friction, and plan for all three. The decline rate you're fighting — 30 to 40 percent across iGaming globally — is not about you. It's about the category. Most of the levers you can pull sit on the card side of the stack, not the operator side.

The pre-deposit checklist I actually use before funding any card at a sportsbook

- Confirm the operator is licensed in your jurisdiction and shows Mastercard on the cashier list

- Use a debit card on a tokenised mobile wallet rather than a raw credit card PAN when possible

- Run a small first deposit and verify how your issuer codes it — purchase or cash advance — before scaling

- Check that the cashier offers Mastercard as a withdrawal method, not just a deposit method

- If the operator settles cross-border, expect a foreign-transaction surcharge even on a home-currency amount

- Never fund a bet with credit you cannot pay off in full at the next statement cycle

If you remember only one line from this breakdown, make it the last bullet.