Mastercard Gift Cards and Sportsbooks: The Bookmaker's Cashier Dilemma

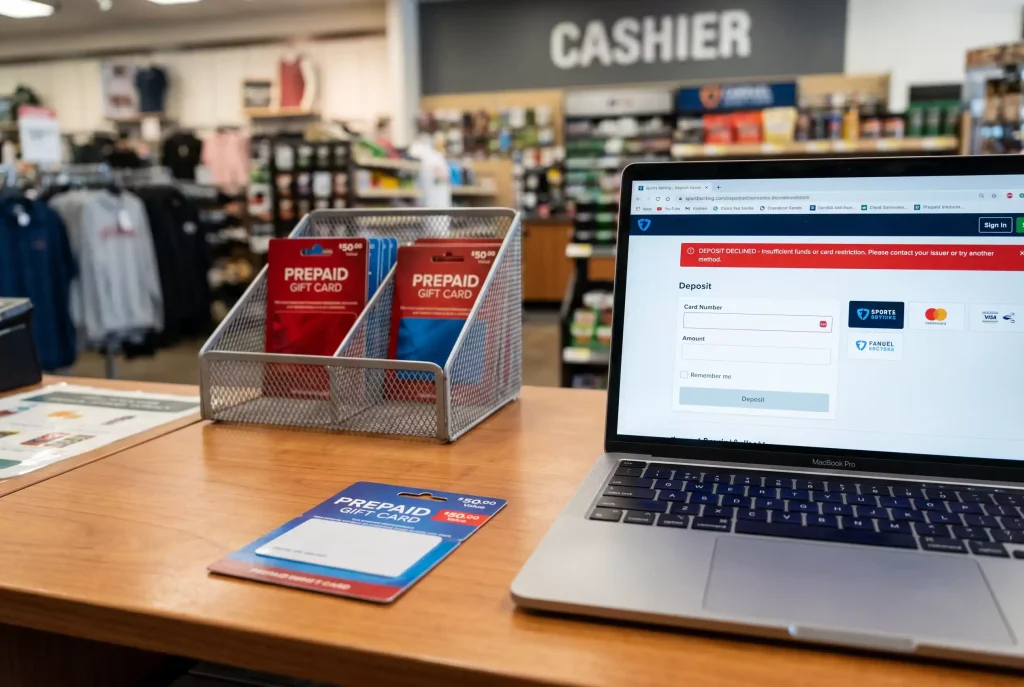

The $100 Mastercard gift card that died at the cashier

A reader in Melbourne once spent a Saturday afternoon trying to deposit a $100 Mastercard gift card at four different Australian-licensed operators. All four cashiers accepted the 16-digit number, all four accepted the CVV, all four moved him to the 3D Secure prompt, and all four returned an identical “card not supported” message after the authorisation call. His conclusion, reasonable enough, was that sportsbooks hate gift cards. The truth is more specific and more useful: gift cards fail for structural reasons that operators cannot override, no matter how much a cashier would like to take the money.

A Mastercard gift card looks like any other Mastercard when you hold it in your hand. The network logo is there, the chip is there, sometimes even a contactless symbol. Under the hood the product is built to do three things — sit on a shelf, get spent once, and disappear. Everything about a sportsbook deposit pushes against that design. In this piece I walk through why cashiers refuse these cards, what the BIN table actually sees, how KYC and AML treat a non-personalised card, and which payment rails behave similarly enough to deserve the same warnings.

Gift cards versus reloadable prepaid — the difference that matters

Both categories sit under the prepaid umbrella, so readers assume they behave the same way. They do not. A reloadable prepaid Mastercard is tied to a verified cardholder, carries a real billing address, can accept a reload from linked bank accounts or payroll, and frequently shares its BIN range with conventional debit products. A gift Mastercard — Vanilla, OneVanilla, Happy, Gift of Choice, supermarket-branded — is issued to a generic non-personalised profile, carries no real billing address beyond the state or country of purchase, cannot be reloaded, and sits on BIN ranges the network flags specifically as “gift prepaid”.

That BIN distinction is the silent killer. When a sportsbook cashier submits a deposit for authorisation, the risk engine runs a lookup against the first six digits of the card number. For a debit or credit BIN the engine scores the transaction normally. For a reloadable prepaid BIN the engine applies additional scrutiny but usually approves. For a gift prepaid BIN the engine in most cases returns an outright block before the authorisation call even reaches the issuer.

There is also a regulatory lens. Anti-money-laundering frameworks in the US, UK, EU and Australia treat personalised and non-personalised prepaids differently. The personalised reloadable sits inside the normal KYC chain. The non-personalised gift card sits in a bucket regulators worry about — anonymous value that can be moved into a gambling account, won back, and converted to a different cashout method. Operators know this, and their compliance teams set the default answer to “no”.

Why cashiers reject gift cards — the layered block

The rejection is rarely a single decision. It is a stack of filters, and the gift card usually trips at least three of them.

The first filter is the operator’s own deposit rules. Every sportsbook maintains a list of accepted instruments, and most explicitly exclude gift cards, either by wording (“we accept personalised debit and credit Mastercards”) or by BIN exclusion lists maintained by the payment processor. The cashier may not surface this wording, but the rule executes silently the moment you submit the card.

The second filter is the acquirer’s risk engine. This is where the iGaming decline rate of 30 to 40 percent against 5 to 10 percent for ordinary e-commerce comes from. Gift prepaids sit in the highest-risk bucket the acquirer tracks, and many processors configure their engines to auto-decline any gift BIN on any gambling MCC. Operators cannot override an acquirer-level block; they either change processors or accept the rejection.

The third filter is the issuer. Even if the first two filters pass, the issuer of the gift card has its own rules. Many gift-card issuers deliberately exclude MCC 7995 and MCC 7801 from their card programme, which means the authorisation call returns declined regardless of what the sportsbook or the acquirer wanted. This is usually printed, in very small type, somewhere on the back of the card: “not valid for gambling or casino transactions”.

The fourth, subtler filter is 3D Secure. When the authentication step prompts the cardholder to verify, a gift card has no enrolled identity to verify against. The step either skips entirely — a flag in itself — or fails on any phone-based challenge because there is no registered cardholder phone number.

BIN-level restrictions and what the cashier actually sees

If you have ever wondered what a sportsbook’s payment engine literally reads from your card, the answer is a compact structured record. The Merchant Category Code path for regulated operators in the US is MCC 7801, set aside for “Internet Gambling — US Region Only”; legacy and international operators ride on MCC 7995. When a gift Mastercard is presented, the first six digits identify the issuing programme, and that programme’s metadata tells the engine whether the card accepts 7801, 7995, neither, or both.

Most retail gift cards are programmed to accept general-purpose retail MCCs and to decline gambling, adult-content and money-transfer MCCs. This is a decision the programme manager makes at card-issue time, and it applies to every card the programme produces. The cashier does not see the decision — it sees a “do not honour” or “restricted merchant” response code and moves on.

A useful test is to attempt a small authorisation at a different MCC first. If a $1 hold at a general retail merchant authorises but a $10 sportsbook deposit declines, the BIN-level gambling exclusion is almost certainly the cause. A card that declines everywhere is a different problem — typically insufficient balance, expiry, or a dormant account freeze.

Worth noting: even on the rare gift programme that does accept MCC 7801, many US operators impose operator-side caps on prepaid deposits as part of their own responsible-gambling configuration. I have seen a gift card authorise at $20 and decline at $200 on the same cashier in the same minute. The acquirer approved both, the issuer approved both, and the operator’s own rules blocked the larger transaction.

KYC, name match and the awkward gift-card problem

Regulated sportsbooks are required to verify the identity of every account holder and to confirm that deposits come from a source the account holder legitimately controls. That verification is the Know-Your-Customer chain, and it runs every time a new payment instrument is added. Gift cards break the chain in a structural way.

On a personalised Mastercard the cashier sees a cardholder name, a billing address, and — for 3DS2 — a registered contact method. The operator runs a name match against the account’s legal name, a fuzzy address match against the KYC-verified address, and a velocity check against the cardholder’s usage history. Pass all three and the deposit clears. On a gift card none of this exists. The cardholder name is typically “Valued Customer” or blank. The billing address is the retailer’s distribution centre. The velocity history is zero because the card was bought yesterday.

Mastercard corporate has been vocal about misuse of its network for unauthorised gambling payments. A spokesperson told PYMNTS in March 2025 that Mastercard has zero tolerance for illegal activity on its network and is investigating the sites in question. That posture translates into real operational pressure on acquirers, who in turn lean harder on operators to reject anonymous-feeling instruments. Gift cards get caught in the mesh because they look, to the compliance engine, exactly like what a motivated bad actor would use.

The result for a legitimate bettor trying to use a gift card is predictable. Even if the cashier accepts the deposit, the first KYC trigger — typically the first withdrawal, or a cumulative deposit threshold — stalls the account while compliance asks for documents that cannot be produced. How that full chain of checks unfolds when you present a Mastercard is covered in detail in this guide to what sportsbooks verify behind the scenes with your card, which is worth reading if you want to understand why a seemingly clean deposit sometimes triggers a freeze days later.

Alternatives that behave like gift cards but actually work

If the appeal of a gift card is the fixed-amount bankroll — load it, spend it, stop — several legitimate rails replicate that behaviour without the BIN-level block.

The most direct is a bank-issued personalised reloadable Mastercard used as a dedicated betting card. You open a second account at a challenger bank, fund it from your main account to a capped amount, and use the debit Mastercard attached to that account. The risk profile from the operator’s perspective is identical to any normal debit card, but your bankroll is ring-fenced at the account level.

Play+ is the purpose-built option in the US market. It is a prepaid programme specifically designed to work with regulated sportsbooks, funded from a linked bank account or a credit/debit card, and it passes cashier checks reliably because the issuer has built the MCC approvals into the programme. Play+ behaves like a gift card in the sense that you load a known amount, but it is personalised and reloadable and it clears payouts back to the same card.

For readers outside the US, bank-issued travel money Mastercards serve a similar role. These are reloadable, personalised, and on debit-style BIN ranges that sportsbooks accept by default. The catch is cross-border fees and currency conversion, which I address in a different article.

The quick rule I give readers who ask “can I just use a gift card?”: if the real motivation is ring-fencing a small bankroll, use a dedicated debit account or Play+. If the real motivation is anonymity, the cashier is structurally designed to say no, and there is no workaround worth the effort.