Australia's 2024 Credit Card Gambling Ban and Mastercard: The New Rules in Practice

The Tuesday when half of Australia’s card deposits stopped working

On Tuesday 11 June 2024, Australia’s ban on credit cards, credit-related products and digital currency for online wagering came into force — and in the 48 hours either side of that date, compliance teams at every licensed Australian operator were awake at ungodly hours validating that their cashier code was actually doing what the regulator had required. I watched two of those rollouts closely. One operator flipped the switch cleanly at 00:00 AEST. The other had a 40-minute window where the code deployed but the BIN lookup table had not refreshed, and a handful of credit Mastercards slipped through until the team caught it.

For Australian bettors, June 2024 was the moment a legitimate cashier convention of fifteen years quietly ended. Credit-card deposits at licensed Australian operators went from normal to illegal overnight, and the mechanism for enforcement — cashier-level BIN checks and issuer-side declines — was in place before most players even noticed. Eighteen months on, the rules have bedded in, the penalty framework has been tested in practice, and the operator cashier has settled into a new steady state. This piece walks through what the ban actually covers, the penalty structure that gives it teeth, how BetStop connects to card-level enforcement, why debit Mastercards continue to work cleanly, and what has changed in operator cashier flows since the rollout.

What the ban actually covers

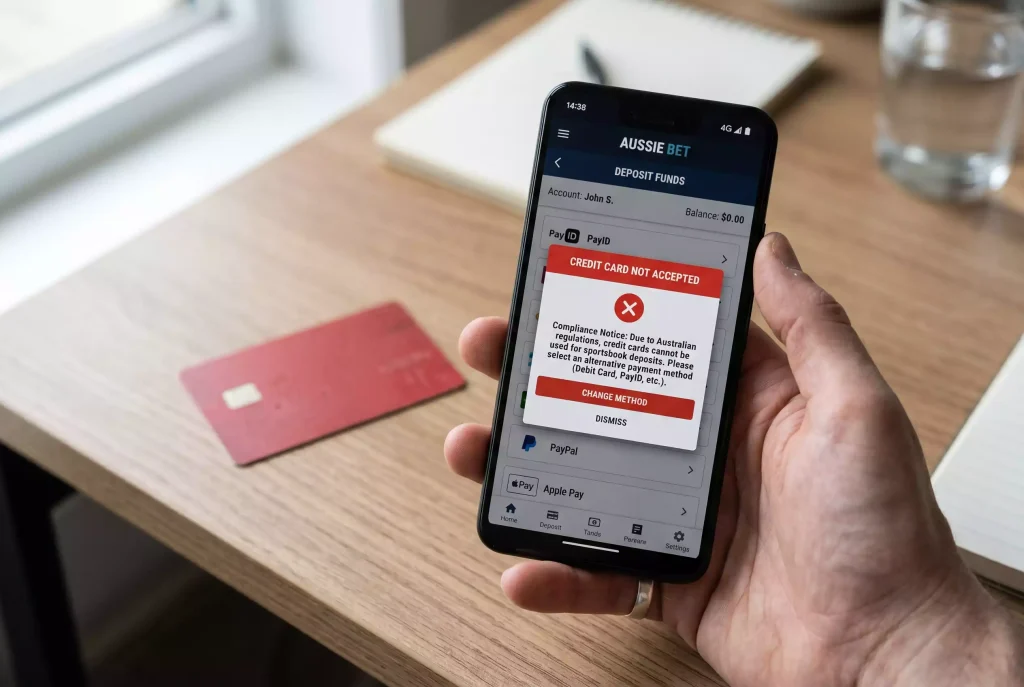

The Interactive Gambling Act amendments that implemented the ban prohibit Australian-licensed wagering service providers from accepting deposits from credit cards, credit-related products, and digital currency for online wagering. The scope is comprehensive — the ban covers sports betting, race wagering, and every other product inside the licensed wagering framework.

The “credit-related products” language is what separates Australia’s rule from earlier attempts in other jurisdictions. It captures not just credit cards but any instrument that draws from credit at any point in its funding chain. A Mastercard credit card is in scope. A prepaid Mastercard loaded from a credit card is in scope. An e-wallet funded from a credit facility is in scope. A buy-now-pay-later linked deposit is in scope. The regulator wrote the rule broadly to prevent the workarounds that partial bans in other markets had allowed.

Digital currency is also captured. The rule prohibits deposits made directly from cryptocurrency or from instruments denominated in digital currency, applying the same principle — that gambling should not be funded from sources the bettor does not currently hold as liquid personal money. The scope here has been less tested in practice simply because crypto represented a small share of Australian licensed deposits before the ban.

Debit Mastercards are explicitly outside the ban. Deposits from a bank-account-linked debit Mastercard — drawing directly from the bettor’s own available money — remain fully legal at licensed operators. This is the workhorse rail for Australian sports betting in 2026, and the data reflects it: since the ban came in, debit card transactions have become the dominant card-based deposit path.

The penalty structure that makes compliance universal

The penalty for a licensed operator accepting a prohibited credit-related deposit is up to AU$234,750 per contravention — roughly US$155,085 in early-2026 conversion terms. The unit of measurement is critical. It is per contravention, not per enforcement action, which means a single operator with a cashier bug that allowed a hundred prohibited transactions before being caught could theoretically face a penalty of over AU$23 million.

The Australian Communications and Media Authority, the regulator charged with enforcement, has been pragmatic about applying the ceiling. Formal enforcement actions have focused on systemic failures rather than isolated incidents, and operators who have flagged an error themselves and remediated quickly have generally faced formal warnings rather than monetary penalties. But the ceiling is there, and it concentrates compliance teams’ minds.

The political framing behind the ban has been blunt. The responsible minister at the time said simply that Australians should not be gambling with money they do not have, and that statement has been quoted repeatedly in the eighteen months since as the shorthand justification for the rule. Industry bodies themselves have acknowledged the measure’s consumer-protection rationale; the chief of the Responsible Wagering Australia trade body publicly described the policy as an important measure to protect customers and help them stay in control of their gambling behaviour.

The result is near-universal operator compliance. Every licensed Australian wagering provider has updated its cashier to reject credit Mastercards, credit-related wallets and digital-currency deposits by default. The technical implementation is straightforward — a BIN lookup at the start of any deposit flow identifies the card type, and credit and credit-linked products are rejected before the authorisation call.

BetStop and the card-level enforcement link

BetStop, Australia’s national self-exclusion register, launched in August 2023 — ten months before the credit card ban — and the two frameworks now reinforce each other at the cashier. Since BetStop’s launch, more than 22,000 Australians have registered for self-exclusion from licensed online wagering, and the register is checked at every account creation and every deposit by every licensed operator.

The enforcement link with Mastercard works through the operator rather than through the card network. BetStop does not interact with Mastercard directly; it maintains a register of individuals who have chosen to exclude themselves, and operators are required to refuse service to anyone on the register. At the cashier level, the check is identity-based — the operator verifies that the account holder is not on the register — but because Mastercard name-match is part of the cashier KYC chain, the effect is that a self-excluded individual cannot deposit at a licensed operator even using a card in their own name.

The register also interacts with the credit card ban in a subtle way. Someone on BetStop cannot deposit at all at licensed operators, so the credit-card question does not arise for them. But the register’s reach — like the ban’s — stops at the Australian-licensed perimeter. A self-excluded individual attempting to deposit at an offshore book is subject to the offshore operator’s own policies, not BetStop’s. The full mechanics of how BetStop interacts with your card and what it does and does not cover sit in this piece on how Australia’s self-exclusion register blocks card deposits.

Debit Mastercards still work — and better than before

The ban has made debit Mastercards more valuable, not less, in the Australian market. With credit and credit-related products off the table, the debit card has become the default instrument at most licensed cashiers, and operators have invested in making the debit flow faster and more reliable.

Approval rates on Australian-issued debit Mastercards at domestic licensed operators are now among the highest in any market I track. The combination of a cleaner regulatory framework, more focused operator integration, and an issuer base that treats MCC 7995 debit transactions as routine has pushed the approval rate for clean accounts into the mid-90s. Compare this to the industry-wide iGaming decline rate of 30 to 40 percent and the Australian debit corridor stands out as an anomaly on the low-decline side.

The Mastercard Send rail has also become more visible in the Australian payout experience. Operators that previously offered card payouts only as a slow fallback have invested in fast card payouts as a competitive feature, and for a typical Australian bettor on a verified account, a debit Mastercard payout now lands in minutes rather than the days it took in 2022.

The one area of awkwardness is prepaid. Prepaid Mastercards sit in a grey zone. A prepaid loaded from a bank current account is outside the ban; a prepaid loaded from a credit card is inside it; a prepaid loaded from an unclear source triggers operator caution. Many Australian operators have simplified by restricting prepaid acceptance altogether rather than trying to validate the funding history.

Operator cashier updates since June 2024

The visible cashier changes in Australia since the ban fall into several predictable categories, and they match what other regulated markets have seen when similar rules were introduced.

Card-type detection at registration is now universal and transparent. When a bettor adds a new Mastercard, the cashier displays the card type — debit, credit or prepaid — and rejects credit on the spot with a clear message. The friendliness of the messaging varies by operator; some operators explain the regulatory reason, others simply say “credit card deposits are not supported”.

Funding-source checks on prepaid cards have tightened. Operators that still accept prepaid Mastercards now routinely query network metadata about the card’s funding history and will reject a prepaid that shows credit-card loads. The check is not perfect — metadata visibility varies by issuer — but it catches most of the obvious workarounds.

E-wallet funding-source declarations have been added to several cashiers. When a bettor uses PayPal or a similar wallet to deposit, some Australian operators now present an additional question asking the user to confirm the wallet is not funded from a credit source. This sits at the edge of what an operator can reasonably verify, and the question functions partly as a compliance-documentation device rather than a substantive check.

Affordability checks have tightened in parallel. With credit off the table, the other main vector for harm-linked spending is sustained deposits from a debit account that the player cannot afford. Australian operators have responded with more prominent affordability prompts at threshold amounts and more active monitoring of deposit patterns against declared income. The combined effect with the credit ban is a cashier that is more intrusive than it was in 2023 but also more clearly focused on harm reduction.