When Mastercard Fails at a Sportsbook: Play+, PayPal, ACH and Crypto Ranked

The night my Mastercard failed and cost me a six-leg parlay

A few seasons ago I watched a first-half pick disappear while the cashier spun on “processing” for three straight minutes. The Mastercard was clean, the operator was legitimate, the deposit amount was routine — and something in the fraud stack decided no, not tonight. By the time I gave up, opened PayPal, and came back to the cashier, the line had moved two points in the wrong direction and the parlay was no longer available at the number I wanted. That was the night I stopped treating Mastercard as a single-rail dependency and started maintaining a deliberate backup stack.

Cards in aggregate remain the dominant deposit rail in online sports betting — in 2024 credit and debit cards accounted for roughly $66 billion in online sports betting deposits, the leading share of the total. But dominance does not mean monopoly, and for a bettor whose Mastercard has failed at a specific cashier for specific reasons, the alternatives matter. This piece ranks Play+, PayPal, ACH and crypto in the order that usually makes sense for a US bettor whose Mastercard has just failed, walks through when each is the right call, and closes with a decision matrix.

Play+: the closest thing to a Mastercard without the baggage

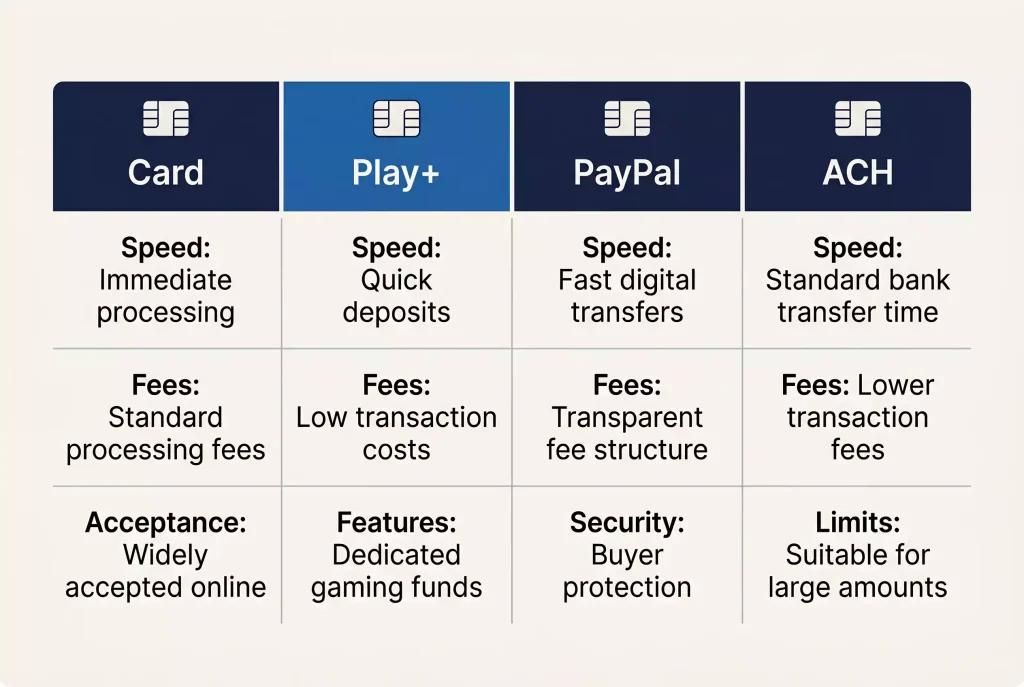

Play+ is a prepaid account programme purpose-built for the US regulated sports-betting and casino market. Operators offer it as a native deposit option, and it often doubles as a payout rail. A Play+ account is opened through the operator, funded from a linked debit card or ACH, and then used to deposit to the sportsbook balance in a single click.

The advantage over Mastercard is that Play+ was designed with gambling MCCs in mind. The approval rate at a gambling cashier is near 100 percent because the rail exists specifically for that purpose; there is no issuer-side decline pattern because the Play+ issuer is not making a gambling-specific judgement on every transaction. Funding the Play+ account itself can hit the same issuer rules that affect Mastercard directly, but once the Play+ balance is established, deposits from it are routine.

Payouts back to Play+ are typically fast. Most major operators treat Play+ as a preferred payout rail, and winnings can land on the Play+ balance in minutes. From Play+ the bettor can move funds to a linked bank account (usually 1 to 3 business days via ACH) or to an eligible card (minutes).

The disadvantage is that Play+ exists mainly in the US and only at regulated operators that have integrated it. International users cannot use it at all, and offshore operators do not offer it. For the US bettor whose specific problem is a declined Mastercard at a regulated domestic operator, Play+ is usually the right answer — and technically its underlying card is often a Mastercard-branded prepaid, meaning the bettor who rejected “Mastercard” as a failed rail has sometimes fallen back to exactly the same network through a different access layer.

PayPal and the e-wallet stack

PayPal has broader reach than Play+ and works across both US and international regulated operators. The account is typically funded from a linked bank account or card, and sportsbook deposits through PayPal are instant. Payouts back to PayPal are also generally fast.

The approval rate for a PayPal deposit at a sportsbook cashier is higher than for a direct Mastercard entry, though not quite as high as Play+ at US regulated operators. PayPal’s underlying funding sources face the same issuer rules — a credit-card-funded PayPal deposit to gambling can be declined at the card level, particularly in markets with credit-card restrictions — but debit-card-funded PayPal and bank-funded PayPal clear reliably.

The KYC step at a sportsbook for PayPal deposits differs slightly from Mastercard. PayPal has its own identity verification, and the operator often accepts a PayPal-verified identity as supporting documentation for KYC. This can speed the account setup process for new bettors, though it does not replace the operator’s own KYC chain.

The downside is that PayPal is not available at every operator, and at some operators it is available for deposits but not for withdrawals. Before committing to PayPal as a primary rail, test that both directions work — a deposit path that fails on withdrawal forces a second rail for payouts and complicates the account setup.

Skrill and Neteller serve similar roles in international markets, particularly for European bettors using international-licensed operators. The functional profile is broadly similar to PayPal, though acceptance at US regulated operators is more limited. For a US bettor on a domestic regulated book, PayPal is typically the preferred e-wallet; for an international bettor on a European book, Skrill and Neteller are more common.

ACH and the bank transfer route

ACH — the US bank-to-bank transfer system — is the slowest of the major rails but also the cheapest and most reliable. An ACH deposit at a sportsbook draws directly from the bettor’s bank account and typically posts to the betting balance within 1 to 3 business days.

The approval rate on ACH is essentially 100 percent for verified accounts with sufficient funds. There is no issuer-side gambling rule because the transfer is a bank-to-bank movement rather than a card authorisation. The underlying risk scoring happens on the operator’s side — the sportsbook runs its own fraud checks on the bank account — but network-level decline patterns do not apply.

The disadvantage is speed. A Mastercard deposit posts in seconds; an ACH deposit posts in 1 to 3 business days. For a bettor who wants to place a bet before a game starts, ACH is not a real-time option. It is the right call for pre-planned bankroll funding, not for impulse or in-game deposits.

Payouts via ACH are slower still. A withdrawal that would land on a debit Mastercard in minutes via Mastercard Send takes 3 to 5 business days via ACH, and the operator’s review queue adds its own time on top. For payouts, faster rails are almost always preferred when they are available.

ACH is the right call for a first deposit at a new operator where the bettor wants to verify the operator is legitimate before committing real-time funds. The slower pace gives breathing room to check operator behaviour, and the bank-level visibility gives the bettor better protection if something goes wrong.

Crypto rails where legal

Cryptocurrency deposits are accepted at some offshore operators and at a growing but still limited set of regulated markets. The US regulated market is generally not crypto-friendly; Australia’s 2024 ban explicitly included digital currency in the restricted category. For US bettors on regulated books, crypto is not typically a primary option.

Where crypto rails are legal and accepted, they offer specific advantages. Deposit and payout speeds are fast — typically faster than ACH, often comparable to Mastercard Send, particularly on newer blockchains optimised for transaction throughput. Fees vary by network and time but are often competitive with or cheaper than card-based rails. The settlement is generally final on receipt, which reduces chargeback risk for the operator and therefore reduces the risk-scoring overhead on transactions.

The disadvantages are substantial. Crypto prices are volatile, which means a deposit made in crypto is exposed to price movement between deposit and conversion. Most operators convert crypto to fiat on receipt, but some hold crypto-denominated balances, and the exposure matters. The consumer protection framework on crypto transactions is weaker than on card transactions — no chargeback equivalent exists for a reversed crypto payment, and the KYC chain varies widely by operator. The iGaming decline rate context (30 to 40 percent on cards) does not apply to crypto, which has very high acceptance, but the consumer protections that come with cards are also absent.

For bettors in markets where crypto is legal and where their preferred operator accepts it, crypto can be a useful rail. For most US regulated market users, it is not a practical alternative to Mastercard because their regulated operators do not accept it.

Decision matrix by use case

The right rail depends on what specifically failed about Mastercard and what the bettor needs next. A few patterns are worth naming.

If the Mastercard failure is an issuer-side gambling block — the issuer is declining all MCC 7801 or 7995 transactions — then Play+ at a US regulated operator is usually the cleanest alternative. The Play+ account is funded from a debit card or bank account that does not face the same gambling-block issue, and the sportsbook deposit from Play+ does not go through the blocked issuer.

If the Mastercard failure is fraud-engine scoring — the transaction is being flagged as high-risk by the Mastercard network or the issuer — then PayPal with a tokenised biometric confirmation often clears. PayPal’s own fraud scoring runs differently from Mastercard’s, and a transaction that the Mastercard engine flagged may clear cleanly through PayPal.

If the Mastercard failure is event-weekend infrastructure overload — the cashier is timing out during peak load — the answer depends on urgency. If the bet can wait, ACH avoids the peak-load cashier entirely. If the bet cannot wait, trying Apple Pay or Google Pay with the same Mastercard often succeeds because tokenised wallet flows use different cashier paths that were provisioned for peaks.

If the Mastercard failure is persistent across multiple attempts and operators, the problem is likely bank-side rather than operator-side, and switching cards rather than switching rails is the right move. Call the issuer, ask specifically about MCC 7995 and MCC 7801 acceptance, and either change product or change bank. A full treatment of how US issuers treat gambling MCCs sits in this analysis of which US issuers routinely block sportsbook Mastercard deposits and how their policies differ.

The meta-rule across all of this: maintain more than one deposit path set up in advance. A bettor with a Mastercard, a PayPal account, and an ACH link ready to go has three ways to deposit; a bettor with only a Mastercard has one. The setup friction of adding additional rails is a one-time cost; the friction of setting them up at 4pm on Super Bowl Sunday is a substantial cost at exactly the wrong moment.