Mastercard in Mobile Sportsbook Apps: Apple Pay, Google Pay and Tokenised Deposits

The 30-second deposit that changed my Saturday routine

The first time I deposited at a sportsbook through Apple Pay with my Mastercard tokenised in the wallet, the entire flow took 30 seconds from opening the app to the balance update. No typing a card number, no 3D Secure redirect, no waiting for an SMS code. The Face ID check confirmed my identity, Apple Pay handed the tokenised card to the operator, and the deposit posted before I had put the phone down. The experience was a meaningful step up from entering a 16-digit number plus expiry plus CVV plus authentication — enough to shift my default deposit method within a week.

Mobile has become the dominant channel in sports betting. Mobile betting made up 84 percent of all US wagers in 2025, and for the 18 to 34 age cohort the share using mobile apps as the primary platform sits above 85 percent. The deposit infrastructure has evolved to match. Tokenised mobile-wallet deposits through Apple Pay and Google Pay with Mastercard underneath have become the default for serious bettors, and the cashier experience is materially better than direct card entry for both speed and approval rate. This piece walks through how mobile tokenisation actually works, how Apple Pay and Google Pay deposits behave at sportsbooks specifically, why wallet deposits approve more often, and what the biometric confirmation flow adds.

How mobile tokenisation works

When a Mastercard is added to Apple Pay or Google Pay, the wallet service requests a token from the Mastercard network. The token is a different 16-digit number from the underlying card number, cryptographically bound to the specific device, and useable only through that wallet. The original card number stays on the user’s physical card and in the issuer’s records; the token is what actually moves through the network when the wallet is used.

The tokenisation standard is called EMVCo Payment Tokenisation, and it produces several security benefits. If the token is intercepted, it cannot be used outside the specific device and wallet. If the underlying card is compromised, the token is not affected. And transactions made with the token carry signals the network can use to score them — notably that the transaction originated from a registered device with a registered biometric, both of which reduce fraud risk.

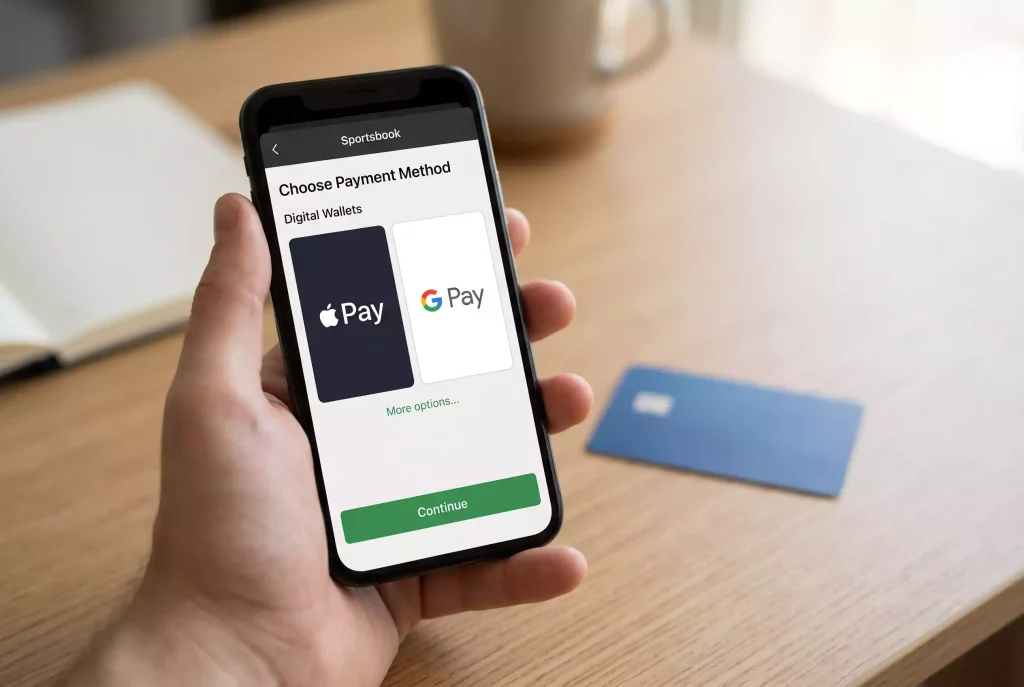

For a sportsbook deposit through Apple Pay, the flow is: the user taps “deposit” in the app, selects Apple Pay, confirms the amount, and completes Face ID or Touch ID. Apple Pay hands the tokenised card details to the sportsbook’s cashier, which submits them to the Mastercard network as a standard authorisation with a tokenised PAN. The network and issuer see the token, recognise it as a registered wallet credential, and approve based on the same logic as a regular card transaction plus the additional assurance the tokenisation signals.

The whole flow completes in 1 to 5 seconds. The user’s experience is a biometric check and a success confirmation; the underlying network exchange is invisible. Contactless payment technology more broadly is now 59.2 percent of transactions in North America, and the rails that power contactless retail payments are the same rails that carry tokenised sportsbook deposits. The infrastructure is mature.

Apple Pay with Mastercard at sportsbooks

Apple Pay is the tokenised wallet option for iPhone and iPad users, and support at major US sportsbooks is now near-universal. Every tier-one US operator supports Apple Pay deposits with a Mastercard, and the integration has been stable for years.

The cashier flow from the user’s perspective is optimised for speed. Opening the sportsbook app, selecting Apple Pay as the deposit method, confirming the amount, and completing Face ID or Touch ID takes 10 to 20 seconds total. The confirmation screen shows the deposit as successful before the user has switched out of the app.

The behind-the-scenes approval rate on Apple Pay deposits is higher than on direct card entry for the same underlying card. Several factors contribute: the biometric check provides strong authentication (often more robust than SMS-based 3D Secure), the device fingerprint is well-established for repeat users, and the token carries signals that mark it as a registered wallet credential. A Mastercard that would have faced a 30 to 40 percent decline rate on direct entry can see a 10 to 20 percent decline rate when tokenised through Apple Pay.

Apple Pay also handles 3D Secure natively. Where a direct card entry might redirect the user to a 3DS challenge screen, Apple Pay completes the 3DS step through the device’s biometric check. This is faster and, importantly, more reliable — SMS-based 3DS challenges can fail if the SMS is delayed or the authentication method is unavailable, while the biometric check is always available to the user unlocking their own device.

Deposit limits under Apple Pay match the underlying card’s limits. The wallet does not impose its own cap; if the underlying Mastercard supports a $5,000 authorisation, Apple Pay carries the same limit. The wallet is a transport mechanism for the card, not a substitute for it.

Google Pay with Mastercard at sportsbooks

Google Pay is the tokenised wallet for Android users, and the experience is functionally equivalent to Apple Pay at the sportsbook cashier. Support at major US operators is similarly universal, with some nuances around older Android versions.

The Google Pay flow mirrors Apple Pay’s: select Google Pay in the cashier, confirm the amount, complete biometric or PIN authentication, see the confirmation. The speed is comparable, the approval rate is comparable, and the security profile is comparable.

One specific difference: Google Pay handles the 3D Secure step slightly differently depending on the specific Android version and the issuer’s integration. Most flows complete the 3DS step through the device-level authentication, but a small minority of combinations trigger a full 3DS challenge outside the wallet. This is a minor friction point and affects only a small subset of users.

Google Pay is generally available on the sportsbook’s mobile website in Android browsers as well as in the native app. The experience on the mobile web is slightly less polished than in the app — the flow takes more taps, and the biometric check happens through the browser rather than through the OS — but the end result is the same.

For Android users who have not yet added Mastercard to Google Pay, the one-time setup takes a few minutes through the Google Pay app. After setup, the card is available across every merchant that supports Google Pay, not just the sportsbook. The set-once-use-everywhere pattern is the same as Apple Pay.

Why wallet deposits approve more often

The higher approval rate on tokenised wallet deposits comes from how the Mastercard network scores the transaction. Several signals are present on a wallet deposit that are not present on a direct card entry, and each of them reduces the fraud score.

Device binding is the first. A tokenised card is bound to a specific device with a specific biometric credential. The network knows that the transaction originated from a registered device whose owner completed a biometric check, which is stronger evidence of legitimate use than a card number and CVV entered into a web form.

Authentication quality is the second. A biometric check through Face ID, Touch ID or fingerprint authentication is resistant to most remote-compromise scenarios. A direct card entry with a password or SMS-based 3DS is more vulnerable. The network weights the authentication method in its risk scoring.

Velocity patterns are the third. A wallet that has been used regularly for non-gambling transactions — paying for coffee, online shopping, transit — carries a history that the gambling transaction gets to borrow from. The device is not a fresh environment; it has an established pattern of legitimate use. A direct card entry with a new IP or a new device is scored more cautiously.

The industry-level context adds weight. As AGA leadership has framed it, sports betting belongs under state and tribal regulation as the way consumers are protected and communities share in the benefits. Tokenised deposits fit that consumer-protection framing — they reduce card-compromise risk, they reduce dispute rates, and they raise the barrier to fraudulent account creation. Operators have incentives to promote them, issuers have incentives to approve them, and the network has incentives to invest in the infrastructure.

The approval rate improvement is meaningful at scale. A bettor who faced occasional declines on direct card entry often sees those declines vanish when they move to Apple Pay or Google Pay. Not every user sees the improvement, but the aggregate pattern is consistent. For bettors who want to understand the full set of alternatives to direct Mastercard use — including non-wallet rails that trade off different dimensions — the comparison sits in this look at when Mastercard fails at a sportsbook and how Play+, PayPal, ACH and crypto rank.

Biometric confirmation flow

The biometric step in a tokenised wallet deposit is not cosmetic — it is the single most important authentication event in the transaction. Understanding what it does and does not cover helps explain the security profile.

The biometric check confirms that the person depositing is the person registered with the wallet. Face ID confirms the face matches the enrolment; Touch ID confirms the fingerprint matches; PIN-based fallback confirms the PIN matches. None of these is foolproof — biometric spoofing is a known attack surface — but the combination of device binding, biometric matching and network scoring produces a transaction that is hard to spoof remotely.

What the biometric check does not do is confirm that the person is the rightful owner of the underlying Mastercard. If someone else’s card is added to your wallet (with your consent, through the wallet’s setup flow), your biometric authenticates the deposit even though the card is not yours. This is typically fine for household card use but matters for KYC purposes — the sportsbook’s compliance chain still requires a name match between account holder and cardholder, regardless of which wallet was used.

The authentication flow completes in under 2 seconds for most users. The entire deposit, from tapping the deposit button to seeing the balance updated, typically takes 10 to 15 seconds. This is the fastest deposit experience available on modern sportsbook infrastructure, and once users experience it they rarely go back to direct card entry.