Mastercard Sports Betting State by State: A 2026 US Operator Map

The map that changes every year

The US sports-betting landscape is the closest thing the world has to a real-time regulatory experiment: 50 states making independent decisions about legalisation, 50 regulatory frameworks evolving at different paces, and 50 sets of rules about what payment methods operators can accept. Legal commercial GGR from US sports betting hit a record $16.96 billion in 2025, up 22.8 percent year-on-year, and the handle underneath that revenue was $166.94 billion — growth big enough to attract operator investment into every legal state and several that were not yet legal when 2026 opened.

For a Mastercard bettor, the map is a practical guide to where cards work, where they hit state-specific restrictions, and where the licensed infrastructure is simply absent. This piece walks through the Northeast cluster where the market is most mature, the Midwest cluster where growth has been steady, the South cluster where the patchwork is thickest, the West cluster with its specific features, and the remaining states without legal sports betting.

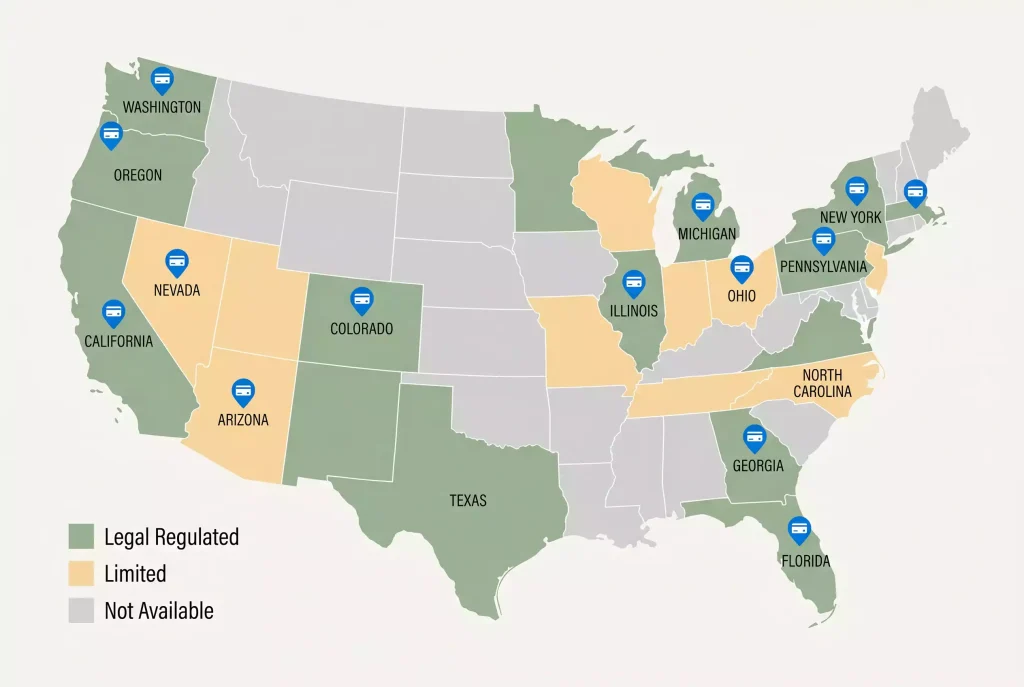

Northeast cluster

The Northeast is the most mature US sports-betting region by any measure — operator count, handle per capita, cashier sophistication. New Jersey, Pennsylvania, New York, Massachusetts, Connecticut, Rhode Island, Maryland, and New Hampshire all have legal regulated sports betting, and all of them see Mastercard acceptance as the default at every major licensed operator.

The approval rates on Mastercard deposits in the Northeast are among the best in any US region. The combination of operator maturity, issuer familiarity with MCC 7801 processing, and the general density of competitive operators means cashiers are well-tuned. A verified account on a mainstream debit Mastercard clears at the high end of the industry approval range. Credit Mastercards run into more variable issuer policy but the structural integration is strong. The 84 percent share of mobile betting across the US in 2025 is particularly pronounced in this region, where the major operators have invested heavily in mobile-app cashier flows.

New York’s market is defined by high tax rates and a concentrated operator set; Mastercard acceptance is uniform but the specific product offerings vary. New Jersey’s longer history produces the broadest payment-method support and the most experienced compliance teams. Pennsylvania has credit-card restrictions on certain gambling products that affect some deposit flows — bettors should check specific operator cashier behaviour on credit deposits.

Mastercard payouts in the Northeast are generally fast. Mastercard Send integration is the default at most tier-one operators, and verified debit Mastercard payouts often land in single-digit minutes for established accounts. Weekend performance is somewhat slower but still competitive with any US region.

Midwest cluster

The Midwest includes several states that legalised relatively recently and several that have been in the market for longer. Michigan, Ohio, Indiana, Illinois, Iowa, and Kansas all have regulated sports betting, with varying degrees of operator presence and Mastercard acceptance.

Michigan and Ohio have the most competitive cashier experiences in the region. Tier-one operators are present in both, and Mastercard acceptance follows the pattern of other mature markets — debit works cleanly, credit is MCC-dependent, prepaid is variable. Indiana and Illinois are slightly less competitive but still see universal Mastercard acceptance at regulated operators.

Iowa is the specific case worth naming. Iowa’s sports betting law restricted credit-card deposits at regulated sportsbooks from launch, meaning that Mastercard credit cards do not work at Iowa-licensed operators regardless of issuer policy. Debit Mastercards work normally. This is one of the few US states with an explicit state-level restriction on credit-card gambling, and it predates the broader industry conversation about credit-card restrictions that has grown louder post-2024.

Kansas and the newer Midwestern entrants are building out their operator presence, and Mastercard acceptance is strong at the operators that have launched. The market depth is less than in Michigan or Ohio, but the payment rails are technically equivalent.

South cluster

The South is the region where the patchwork is thickest. Some states have legal regulated sports betting (Tennessee, Virginia, North Carolina, West Virginia, Louisiana, Mississippi, Arkansas, Kentucky) and others either prohibit it or have not yet legalised it (Texas, Alabama, Georgia, South Carolina, Florida’s situation is contested and evolving).

The AGA’s projection for the NFL season anchored at $30 billion in legal sportsbook wagering across the 2025 season showed the regional concentration clearly, with Southern states contributing a growing share as more legalise. For the legalised Southern states, Mastercard acceptance at regulated operators follows the national pattern — debit is the default, credit is issuer-dependent, prepaid is restricted.

Virginia and Tennessee have mature operator presences by the standards of their state-launch timing, and Mastercard cashier flows are functionally equivalent to those in the Northeast. North Carolina launched more recently and the operator integration continues to mature; Mastercard acceptance is universal but the full feature set (Send-based instant payouts, for example) has been rolling out over time.

The unregulated Southern states are the largest gap in US Mastercard betting coverage. Residents of Texas, Alabama, and Georgia do not have legal sportsbook options in their home state, and many cross state lines to bet in neighbouring states or use offshore operators despite the regulatory risks. Super Bowl weekend tells the story at scale — the 2025 Super Bowl generated roughly $1.39 billion in legal bets, with 68 million Americans participating across legal channels, and the volumes drawn from Southern states that could not host legal operators were a substantial share.

West cluster

The West region is a mixed bag. California has not legalised regulated sports betting, which is the single largest gap in the US national picture. Arizona, Colorado, Nevada, Oregon, Washington, and Wyoming all have legal regulated sports betting with Mastercard acceptance at major operators.

Nevada is the historical home of US sports betting, and Mastercard acceptance at Nevada licensed sportsbooks is well-established. The market structure is different from the post-2018 states — Nevada’s operators are tied more closely to physical casinos — but the cashier technology is current.

Arizona and Colorado have competitive operator markets with tier-one presences and modern cashier flows. Mastercard acceptance follows national patterns, and payout integration via Mastercard Send is the default at major operators.

Oregon’s market is operator-restricted in a state-specific way, with more limited operator options than peer states. Mastercard acceptance at the available operators is standard, but the overall market is thinner. Washington’s market is tribal-first, with more complex structure, and Mastercard acceptance at the available regulated options is functional but less mature than in neighbouring states.

California’s absence from the regulated map is the most consequential single fact in US sports betting. California represents a very large potential market, and the repeated legislative and ballot-measure failures have left the state without a legal operator presence. Residents bet through out-of-state residents’ accounts, through offshore operators, or through the unregulated parts of the ecosystem. Mastercard’s role in these channels is variable — offshore books often do not accept US-issued cards at all, and the cross-border issues raised in how Mastercard behaves at Super Bowl weekend deposit surges apply particularly to large events when California residents try to find legal alternatives.

States without legal sports betting

As of 2026 the states without legal regulated sports betting include California, Texas, Georgia, Alabama, South Carolina, Idaho, Utah, Minnesota, Wisconsin, Oklahoma, Hawaii, Alaska, and a handful of others depending on how partial-legalisation cases (Florida, for example) are classified.

In these states, a US-issued Mastercard has no licensed sportsbook cashier to approve — the regulated option simply does not exist in the state. Residents have three practical paths: travel to a legal state (the most common for residents of Texas, near Louisiana; Georgia, near Tennessee; California, near Nevada), use offshore operators despite the regulatory risk, or abstain.

The Mastercard behaviour at offshore operators from a US-issued card has been covered elsewhere in this series. The short version: offshore acceptance is variable, fraud rates are higher, consumer protection is weaker, and the issuer-side decline rate is elevated because many issuers treat offshore gambling acquirers with particular caution regardless of card type.

The map is changing. Several of the currently-unregulated states have active legislative or ballot-measure campaigns, and the 2026-2028 window is likely to see at least a few additional states legalise. Bettors in a currently-unregulated state who want to wait rather than use offshore options will typically see a legal option appear within a predictable timeframe if the political trajectory holds.