Mastercard Chargeback Reason Codes for Sportsbook Disputes: A Decoder

The three-digit number that decides your dispute before the evidence is read

A reader filed a chargeback in late 2024 under reason code 4837 — “no cardholder authorisation” — against a sportsbook deposit he had personally authorised with 3D Secure and a biometric check. The code was the wrong one, and the wrongness made the dispute fail before the evidence was even examined. Choosing the right reason code is often the whole ball game in a chargeback case, and choosing a wrong one does not just weaken the dispute — it usually kills it outright, because the operator’s evidence package is specifically matched to the code filed.

Mastercard’s chargeback reason codes are a structured taxonomy that tells the issuer, the acquirer, and the merchant what the cardholder is actually claiming. Each code defines the evidence burden, the timeline, and the possible outcomes. For sportsbook disputes, a subset of codes applies — and knowing which fits which scenario is more valuable than any amount of narrative argument. This piece walks through why the code choice matters, the fraud-related codes most relevant to unauthorised deposits, the authorisation-related codes that cover card-present and authentication failures, the cardholder dispute codes for service failures, and which codes sportsbooks almost always win regardless of the cardholder’s claims.

Why reason codes matter at all

The reason code is the operational language of the chargeback system. When an issuer files a dispute, the code tells the network which chapter of the rulebook applies, what the operator must prove, what the cardholder must prove, and what the expected outcome looks like when each side has produced its evidence.

The code is set by the issuer when the dispute is filed, usually based on the cardholder’s description of the problem. A cardholder who says “someone used my card without permission” triggers a fraud code. A cardholder who says “I paid for a service and never received it” triggers a services-not-rendered code. The issuer’s representative does the translation, and the translation is not always perfect — sometimes the chosen code does not match the cardholder’s real grievance, and the dispute then fails on code grounds rather than substance.

The merchant’s response is shaped entirely by the code. A 4837 dispute (no authorisation) requires proof of authentication — the 3D Secure log, the session fingerprint, the device identifier. A 4853 dispute (services not rendered) requires proof of delivery — the deposit crediting to the betting account, the resulting bets placed. The operator assembles different evidence for each, and sending 4837 evidence into a 4853 dispute is a procedural failure.

For a bettor wondering whether to dispute, the first and most important question is not “do I have a case” but “what code fits the case”. If no valid code fits, the dispute will fail no matter how sympathetic the circumstances. If a code fits cleanly, the case is winnable if the evidence supports it.

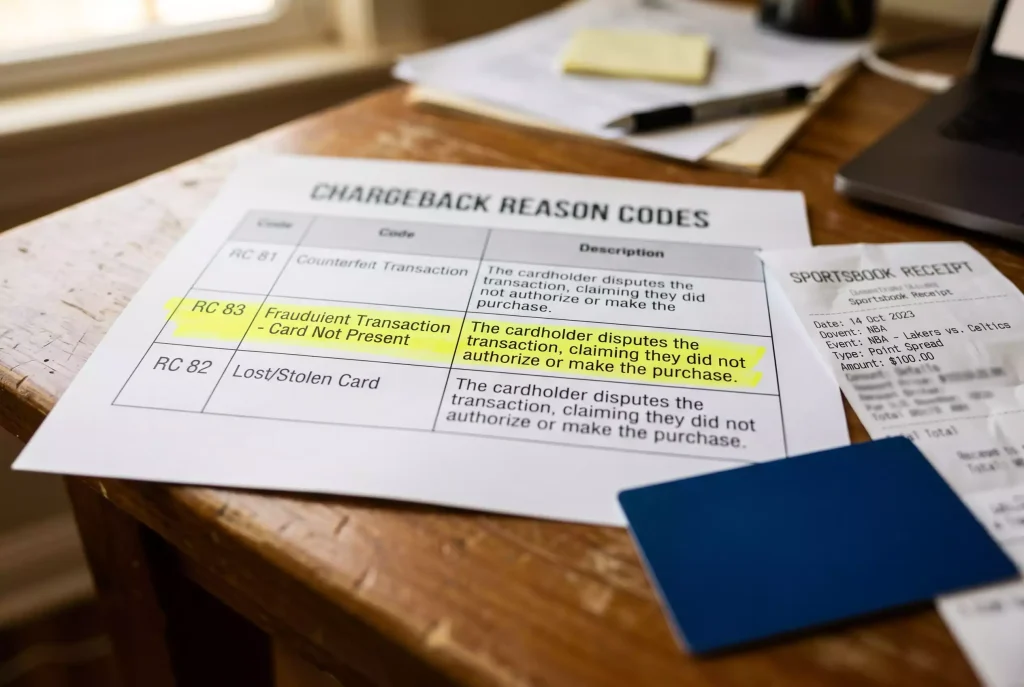

Fraud-related reason codes

Fraud codes apply when the cardholder claims the transaction was not authorised by them and did not benefit them. For sportsbook disputes, three codes dominate this category.

Reason code 4837 — “No Cardholder Authorisation” — is the canonical fraud code for card-not-present transactions. It applies when someone other than the cardholder used the card number and the cardholder had no involvement in the transaction. The merchant’s evidence burden is substantial: they must prove the cardholder authenticated the transaction through 3D Secure, or — if 3DS was not run — that the merchant bore the liability risk and the transaction still should stand on other grounds. For sportsbook deposits, 3DS is almost always run, and the authentication log is usually conclusive evidence that the cardholder did authorise the transaction.

Reason code 4863 — “Cardholder Does Not Recognise — Potential Fraud” — applies when the cardholder sees a transaction on a statement they do not recognise. This is sometimes filed for gambling transactions where the merchant descriptor does not match how the cardholder remembers the operator. Merchants typically defeat these disputes by producing evidence that the descriptor corresponds to a real deposit, though disputes do sometimes succeed when the descriptor is genuinely misleading.

The fraud rate in gambling specifically has been rising. Industry-wide fraud rates grew from 4.2 percent in 2022 to 7.6 percent in 2023, an 80 percent jump, and account takeover attempts make up around 4 percent of all gambling platform login attempts. Legitimate fraud on sportsbook deposits exists and gets successfully disputed, but the burden of proof for the cardholder is high precisely because genuine account takeover is so common that operators have invested heavily in the evidence trail that can distinguish it from friendly fraud.

Authorisation-related reason codes

Authorisation codes apply when there is a problem with how the transaction was authorised in the first place — whether the authorisation was valid, whether it was captured correctly, whether it matched the agreement between the cardholder and the merchant.

Reason code 4834 — “Point-of-Interaction Error” — covers cases where the transaction was processed incorrectly at the point of interaction. For online sportsbooks this might apply if the cashier double-charged the cardholder due to a technical failure, or if the transaction was captured after the cardholder cancelled it. Merchant defence typically requires proving the authorisation was valid and the capture matched the authorisation.

Reason code 4808 — “Authorization-related Chargeback” — applies when a transaction was approved through an incorrect or expired authorisation. For sportsbook deposits this is rare because the transactions are typically authorised and captured simultaneously, but it can apply in cases where an authorisation was reused or held beyond its permitted window.

Reason code 4812 — “Account Number Not on File” — applies when the card number the transaction was charged against does not correspond to an active account. This is usually a technical failure on the acquirer or issuer side rather than a dispute the cardholder would file, but it can surface if a merchant processed against a recycled or invalid card number.

For gambling transactions specifically, the authorisation-related codes intersect with the higher decline rate in the industry. The iGaming decline rate of 30 to 40 percent against 5 to 10 percent in ordinary e-commerce means that many authorisation attempts fail in the first place, and the ones that succeed are a selected subset — which is part of why authorisation-related disputes after the fact are comparatively rare.

Cardholder dispute reason codes

Cardholder dispute codes — sometimes called “quality of service” codes — apply when the transaction was properly authorised but the cardholder claims a problem with what the merchant delivered.

Reason code 4853 — “Cardholder Dispute” — is the catch-all for service failures. It covers services not rendered, services not as described, duplicate charges, and several other sub-categories. For sportsbook disputes this is the code used when a cardholder claims the deposit never appeared in the betting account, or that the operator charged for a service the cardholder did not receive. The merchant’s evidence burden is to prove the deposit was credited and the service was delivered as agreed.

Reason code 4855 — “Non-Receipt of Merchandise or Service” — is narrower than 4853 and applies specifically when the cardholder paid for something and did not receive it at all. For a sportsbook deposit, this applies if the charge hit the card but the betting balance was never credited. Merchants defeat this by producing the cashier log showing the credit.

Reason code 4841 — “Cancelled Recurring Transaction” — applies to subscriptions or recurring charges that were cancelled but continued to bill. For most sportsbook deposits this is irrelevant, but some operators offer subscription-like products (premium access, early data feeds) where it can apply.

The common theme across cardholder dispute codes is that the underlying transaction was authorised — the dispute is about what the merchant did or failed to do afterward. This differs fundamentally from fraud codes, which concern whether the transaction was authorised at all. For sportsbook deposits, the distinction is often the difference between a winnable dispute (service failure) and a futile one (dispute of an authorised deposit that was used to place losing bets).

Which codes sportsbooks rarely lose

Certain reason codes are almost unwinnable for the cardholder on sportsbook disputes because the operator’s standard evidence package conclusively defeats them. Understanding which ones these are helps avoid futile filings.

4837 disputes on deposits that were authenticated through 3D Secure almost always fail for the cardholder. The 3DS log is network-level evidence that the cardholder completed an authentication challenge at the time of the transaction, and the log is cryptographically signed by the issuer itself. When the operator presents this, the issuer cannot credibly claim the cardholder did not authorise the transaction.

4853 disputes claiming non-delivery on deposits that were credited to the betting account fail when the operator produces the cashier log showing the credit. If the cardholder placed bets with the deposited funds, the operator also produces the bet placement records, which further defeats any claim of non-delivery.

Any fraud code on a transaction where the session evidence — IP address, device fingerprint, geolocation — matches the cardholder’s normal pattern fails when the operator submits that evidence. A transaction authorised from the cardholder’s usual mobile phone, at their home IP, using their registered device is very hard to claim as unauthorised without a specific and documented explanation.

Disputes filed after bets were placed and lost — friendly fraud in the canonical sense — fail across every reason code category because the evidence trail always includes the bet placement and the settlement. The operator can produce the bet slips, the game outcomes, and the settlement calculations, all of which establish that the deposit was used for its intended purpose.

The strategic implication for a bettor considering a dispute: if the dispute relates to a losing wager, no reason code will save it. If the dispute relates to a genuine service failure or unauthorised use, choose the code that fits the actual situation, not the one that feels strongest. The wrong code on a valid claim is as damaging as the right code on an invalid claim. Broader context on win rates and operator dispute posture sits in this piece on how Mastercard disputes play out in real sportsbook cases — worth reading before filing to understand what operators typically do with each code type.