Interchange Fees on Mastercard Sportsbook Transactions: Who Actually Pays

The fee nobody on the cashier screen is willing to name

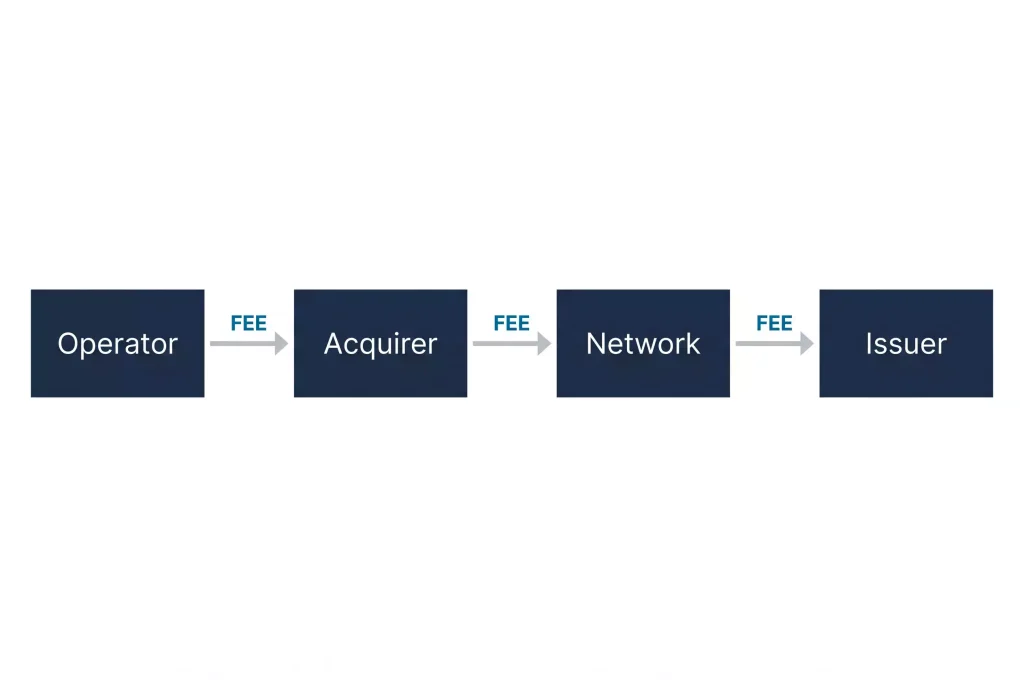

When a bettor deposits $100 at a sportsbook with a Mastercard, only $95 to $97.50 of that deposit actually reaches the operator’s account. The missing $2.50 to $5 is broken up across three parties: the acquirer processing the transaction, the card network carrying it, and the issuer approving it. That tiered fee structure is called interchange, and it is one of the least-visible but most structurally important parts of how card economics shape the sportsbook product you interact with.

Mastercard processed roughly $4 trillion in credit-card purchases in 2023, representing about 21 percent of global credit-card volume, and every one of those transactions carried some form of interchange. Gambling merchants pay higher interchange than retail merchants for reasons that are entirely about risk and profit, not prejudice, and understanding the structure helps explain why operators do what they do at the cashier. This piece walks through what interchange actually is in plain English, what gambling-merchant rates look like, why operators sometimes charge their own deposit fee on top, what the acquirer adds into the stack, and what any of this looks like on the receipt a bettor actually sees.

Interchange in plain English

Interchange is the fee an acquirer pays to an issuer every time a card transaction settles. Think of it as the issuer’s compensation for taking on the credit risk, running the fraud engine, sending the monthly statement, and participating in the card programme at all. The acquirer — the merchant’s bank, effectively — pays the issuer; the acquirer then charges the merchant; the merchant absorbs or passes through the cost.

Interchange rates are set by the card network — Mastercard in this case — and they vary by merchant category, transaction type, card product and geography. A supermarket accepts a contactless debit transaction at a low interchange rate; a small retailer taking a corporate credit card for a large keyed transaction pays a much higher rate. The structure is a matrix of dozens of categories, and the published rate tables run to hundreds of pages.

For a sportsbook, the interchange rate on a typical US-regulated online deposit on a credit Mastercard runs in the range of 2.1 to 2.6 percent of the transaction. On a debit Mastercard the rate is lower — typically 0.5 to 1.0 percent — because debit transactions carry less credit risk and have regulatory caps in several markets. The difference between credit and debit interchange is one reason operators quietly prefer debit deposits even when they do not say so publicly.

Interchange is not profit for Mastercard itself. Mastercard earns its own separate revenue from network fees — smaller percentages on each transaction plus flat fees on data services — and those fees are layered on top of interchange. Mastercard’s FY2024 revenue of $28.167 billion, up 12.2 percent year-on-year, came from this network-fee stream and from adjacent services, not from collecting interchange on its own behalf.

Gambling merchant rates and why they are higher

Gambling merchants pay higher interchange than retail merchants for reasons that are specific to the risk profile of the category. Three factors drive the premium.

The first is chargeback risk. Gambling merchants experience higher rates of cardholder-initiated disputes than most retail categories. Some disputes are legitimate — fraud on a lost card, unauthorised use by a family member — and some are friendly-fraud, where a cardholder who lost a bet attempts to claim the transaction was fraudulent. Regardless of the cause, the chargeback rate drives up the interchange category because the issuer’s cost of handling disputes is real and recurring.

The second is the credit-quality profile of gambling transactions. The iGaming decline rate runs at 30 to 40 percent against 5 to 10 percent in ordinary e-commerce, reflecting the combination of risk rules, MCC-based policies, and cardholder behaviour. Transactions that go through on gambling MCCs are in the subset of attempts that passed risk screening, and the interchange pricing reflects the broader risk profile of the category rather than only the successful transactions.

The third is regulatory overhead. Gambling merchants operate under more complex AML, KYC, and jurisdiction-specific rules than most other categories, and the acquiring side of the transaction carries compliance costs that flow through into pricing. The MCC distinction between 7995 (general gambling) and 7801 (US-regulated internet gambling) exists partly so that the regulated domestic subset can be priced differently from the broader category — and in practice, MCC 7801 interchange sits at the lower end of the gambling range, while MCC 7995 sits at the higher end.

The result is a multi-point interchange premium versus comparable retail merchants. A general retail merchant might pay 1.5 to 1.8 percent on credit interchange; a gambling merchant on the same card at the same transaction size pays 2.1 to 2.6 percent. The difference looks small in percentage terms but is meaningful at scale — every percentage point is substantial revenue at an operator processing billions in deposits annually.

Why operator deposit fees exist

Some sportsbooks charge a flat or percentage-based deposit fee on card transactions; most do not. When the fee exists, it is almost always pass-through of the operator’s own card-processing cost rather than a revenue grab.

The economics are tight. On a credit-card deposit of $100 at 2.5 percent interchange, the operator receives $97.50 net of interchange. On a debit-card deposit at 0.8 percent, the operator receives $99.20. For an operator running thin margins on sports betting — where the theoretical hold might be 6 to 8 percent on balanced books — the 2.5 percent interchange cost consumes a meaningful share of the expected profit before a single bet is placed.

Operators respond in one of two ways. Most operators absorb the interchange cost as part of doing business, reasoning that any explicit fee would drive bettors toward competitors who do not charge one. A minority of operators pass through a deposit fee on credit-card deposits specifically, typically in the 2 to 3 percent range, framed as recovery of the “payment processing cost” without naming interchange directly.

The framing matters because the cardholder’s perception of a fee on a gambling deposit is different from the cardholder’s perception of a fee on a ride-share or a food-delivery. The optics of a fee on top of a product that is already a net cost to most players are poor, and most operators avoid it for marketing reasons as much as economic ones.

In markets where credit-card deposits are banned, the interchange question becomes less pressing because debit interchange is lower and the absorbed cost is smaller. UK and Australian operators post-ban face a structurally cheaper interchange bill than US operators processing credit, and the cashier design reflects that.

Acquirer markup and where the rest of the fee lives

Interchange is what the acquirer pays the issuer, but the acquirer also charges the merchant its own fee on top. This acquirer markup varies enormously depending on the merchant’s negotiating position, the volume processed, and the risk profile of the business.

For a tier-one US sportsbook processing billions in annual card volume, the acquirer markup might be as low as 15 to 30 basis points on top of interchange. For a small or new operator with less negotiating leverage, the markup might be 50 to 100 basis points. The total merchant discount rate — interchange plus network fees plus acquirer markup — therefore lands in the range of 2.5 to 3.5 percent for a typical credit-card deposit at a regulated sportsbook.

The acquirer earns its markup by providing services beyond basic processing: fraud monitoring, chargeback management, reporting infrastructure, and the specialised iGaming compliance support that gambling merchants need. For a new operator entering a regulated market, the acquirer often functions as a compliance partner rather than just a processing conduit, and the markup reflects that value add.

The acquirer market for gambling merchants is smaller than for retail merchants. Fewer acquirers will take on gambling risk, which gives the ones who do more pricing power. This is one of the reasons gambling merchant discount rates have stayed stubbornly high even as interchange in general retail has been compressed by regulatory intervention in several markets.

What the user actually sees on the receipt

The receipt at the sportsbook cashier almost never shows interchange. A $100 deposit appears as a $100 deposit in the user’s account and a $100 charge on the statement. The 2.5 percent interchange and the acquirer markup are absorbed by the operator and never surface to the cardholder.

Where the user does see something is when the operator passes through a deposit fee. In that case the receipt shows the deposit amount and a separate fee line, and the cardholder knows the cost of the deposit. This is the minority pattern in 2026, and it is generally clearly disclosed before the deposit is confirmed.

Cross-border deposits are where the hidden cost can grow more noticeably. A deposit on a foreign-issued Mastercard at a domestic operator often passes through cross-border interchange (higher than domestic) and foreign-transaction fees charged by the issuer to the cardholder. The cardholder may see the issuer’s fee as a separate line on their statement but will not see the cross-border interchange component.

For most bettors using a domestic debit Mastercard at a domestic regulated operator, interchange is simply invisible — and that is by design. The user experience depends on the fee being hidden inside the operator’s cost structure rather than surfaced at the moment of deposit. A closer look at every visible fee line that can appear on a user-facing bill — issuer surcharges, FX markup, and any deposit fee the operator does pass through — sits in this breakdown of every Mastercard fee line on a gambling deposit, decoded.